Albertsons 2012 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2012 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

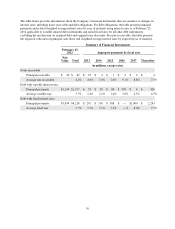

Management expects that the Company will continue to replenish operating assets with internally generated

funds. There can be no assurance, however, that the Company’s business will continue to generate cash flow at

current levels. The Company will continue to obtain short-term or long-term financing from its credit facilities.

Long-term financing will be maintained through existing and new debt issuances and its credit facilities. The

Company’s short-term and long-term financing abilities are believed to be adequate as a supplement to internally

generated cash flows to fund capital expenditures and acquisitions as opportunities arise. Maturities of debt

issued will depend on management’s views with respect to the relative attractiveness of interest rates at the time

of issuance and other debt maturities.

Certain of the Company’s credit facilities and long-term debt agreements have restrictive covenants and cross-

default provisions which generally provide, subject to the Company’s right to cure, for the acceleration of

payments due in the event of a breach of a covenant or a default in the payment of a specified amount of

indebtedness due under certain other debt agreements. The Company was in compliance with all such covenants

and provisions for all periods presented.

In June 2006, the Company entered into senior secured credit facilities provided by a group of lenders consisting

of a five-year revolving credit facility (the “Revolving Credit Facility”), a five-year term loan (“Term Loan A”)

and a six-year term loan (“Term Loan B”). On April 5, 2010, the Company entered into an Amended and

Restated Credit Agreement (the “Credit Agreement”), which provided for an extension of the maturity of

portions of the senior secured credit facilities provided under the original credit agreement. Specifically, $1,500

of the Revolving Credit Facility was extended until April 5, 2015 and $500 of Term Loan B (“Term Loan B-2”)

was extended until October 5, 2015. The remainder of Term Loan B (“Term Loan B-1”) matures on June 2,

2012. On June 2, 2011, the $600 unextended Revolving Credit Facility expired and Term Loan A matured and

was paid.

On April 29, 2011, the Company entered into the First Amendment to the Credit Agreement (the “Amended

Credit Agreement”) which provided for Term Loan B-1 lenders to extend all or a portion of their advances into

either Term Loan B-2 or a new seven-year term loan (“Term Loan B-3”) and also allowed new lenders to

participate in Term Loan B-3. Through the amendment, $86 of Term Loan B-1 was extended into Term Loan B-2

and $161 of Term Loan B-1 was extended into Term Loan B-3. In addition, Term Loan B-3 received $291 of

new advances which were used to reduce short-term borrowings and to retire Term Loan A at its maturity. Term

Loan B-3 matures on April 29, 2018.

The fees and rates in effect on outstanding borrowings under the senior secured credit facilities are based on the

Company’s current credit ratings. As of February 25, 2012, there was $27 of outstanding borrowings under the

Revolving Credit Facility at Prime plus 1.50 percent, Term Loan B-1 had a remaining principal balance of $22 at

LIBOR plus 1.375 percent, all of which was classified as current. Term Loan B-2 had a remaining principal

balance of $577 at LIBOR plus 3.25 percent, of which $6 was classified as current. Term Loan B-3 had a

remaining principal balance of $448 at LIBOR plus 3.50 percent with a 1.00 percent LIBOR floor, of which $5

was classified as current. Letters of credit outstanding under the Revolving Credit Facility were $288 at fees up

to 2.75 percent and the unused available credit under the Revolving Credit Facility was $1,185. The Company

also had $2 of outstanding letters of credit issued under separate agreements with financial institutions. These

letters of credit primarily support workers’ compensation, merchandise import programs and payment

obligations. Facility fees under the Revolving Credit Facility are 0.625 percent. Borrowings under the term loans

may be paid, in full or in part, at any time without penalty.

Under the Amended Credit Agreement, the Company must maintain a leverage ratio no greater than 4.0 to 1.0

from December 31, 2011 through December 30, 2012 and 3.75 to 1.0 thereafter. The Company’s leverage ratio

was 3.47 to 1.0 at February 25, 2012. Additionally, the Company must maintain a fixed charge coverage ratio of

not less than 2.25 to 1.0 from December 31, 2011 through December 30, 2012 and 2.3 to 1.0 thereafter. The

Company’s fixed charge coverage ratio was 2.58 to 1.0 at February 25, 2012.

34