WeightWatchers 2002 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2002 WeightWatchers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

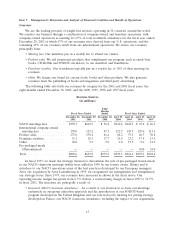

For the fiscal year ended December 29, 2001 cash and cash equivalents decreased $21.2 million, as

the $121.6 million of cash flows provided by operations were used primarily for investing activities.

Cash flows used for investing activities totaled $120.1 million and were primarily comprised of

payments for franchise acquisitions of $84.4 million (including acquisition costs) for our Weighco

franchise and $13.5 million for our Oregon franchise, loans totaling $17.3 million made to

WeightWatchers.com and capital expenditures of $3.8 million. Net cash flows used for financing

activities were $21.4 million and consisted primarily of proceeds from borrowings under our senior

credit facility of $60.0 million, offset by the payment of $1.5 million of dividends on our preferred

stock, payments of $1.0 million associated with the cost of the public equity offering, repayments of

$50.8 million principal on our outstanding senior credit facilities and the repurchase of 6,719,254 shares

of our common stock held by Heinz for $27.1 million.

For the eight months ended December 30, 2000, cash and cash equivalents remained flat at

$44.0 million. Cash flows of $28.9 million were provided by operating activities of which $21.6 million

was used for investing activities and $8.0 million was used for financing activities.

Working capital at December 28, 2002 was $22.1 million compared to a deficit of $24.1 million at

December 29, 2001. The change in working capital was primarily attributable to increases in cash

($34.2 million), prepaid expenses ($9.8 million), accounts receivable ($5.5 million) and inventory

($12.4 million). The increase in prepaid expenses was due to prepaid advertising relating to the spring

campaign and prepaid rents and meeting materials for meeting locations. The increase in accounts

receivable was due to an increase in receivables due from franchises and licensees and the increase in

inventory was the result of the anticipated increase in product sales during the winter diet season. This

was offset by an increase in various current liabilities of $15.4 million, including income taxes

($4.8 million) and deferred revenue and other current liabilities ($10.6 million).

Capital spending has averaged approximately $4.0 million annually over the last three years and

has consisted primarily of leasehold improvements, furniture and equipment for meeting locations and

information system expenditures.

Our total debt was $454.7 million, $474.0 million and $470.7 million at December 28, 2002,

December 29, 2001 and December 30, 2000, respectively. We had approximately $45.0 million of

additional borrowing capacity available under our revolving credit facility as of December 28, 2002 and

December 29, 2001, and approximately $30.0 million as of December 30, 2000. On January 16, 2001, we

acquired the franchise territories and certain business assets of Weighco for $83.8 million. We financed

the acquisition with available cash of $23.8 million and additional borrowings of $60.0 million under

our senior credit facilities.

Our debt consists of both fixed and variable-rate instruments. At December 28, 2002,

December 29, 2001 and December 30, 2000, fixed-rate debt constituted approximately 56.0%, 50.3%

and 51.9% of our total debt, respectively. The average interest rate on our debt was approximately

9.1%, 8.6% and 11.6% at December 28, 2002, December 29, 2001 and December 30, 2000, respectively.

23