WeightWatchers 2002 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2002 WeightWatchers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

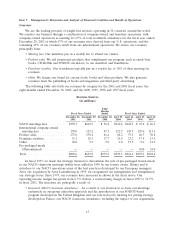

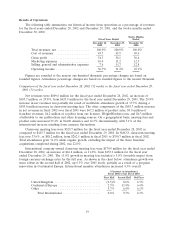

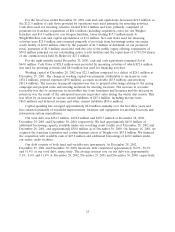

Item 6. Selected Financial Data

The following schedule sets forth our selected financial data for the fiscal years ended

December 28, 2002 and December 29, 2001, the eight months ended December 30, 2000, and the fiscal

years ended April 29, 2000, April 24, 1999, April 25, 1998 and April 26, 1997.

SELECTED FINANCIAL DATA

(In millions, except per share amounts)

Eight

Months

Ended

Fiscal Years Ended Fiscal Years Ended

December 30,

December 28, December 29, 2000 April 29, April 24, April 25, April 26,

2002 2001 (35 Weeks) 2000 1999 1998 1997

Revenues, net .................. $809.6 $623.9 $273.2 $399.5 $364.6 $297.2 $292.8

Net income (loss) ................ $143.7 $147.3 $ 15.0 $ 37.8 $ 47.9 $ 23.8 $(24.0)

Working capital (deficit) ............ $22.1 $(24.1) $ 10.2 $ (0.9) $ 91.2 $ 65.8 $ 64.9

Total assets .................... $609.9 $482.9 $346.2 $334.2 $371.4 $370.8 $373.0

Long-term obligations ............. $454.7 $500.0 $496.7 $500.5 $ 16.7 $ 17.7 $ 71.6

Basic Net income (loss) Per Share:

Income (loss) before extraordinary item $ 1.35 $ 1.37 $ 0.13 $ 0.20 $ 0.17 $ 0.09 $(0.09)

Extraordinary item, net of taxes ..... —(0.03) — ————

Net income (loss) ............. $1.35 $ 1.34 $ 0.13 $ 0.20 $ 0.17 0.09 $(0.09)

Diluted Net Income (Loss) per Share:

Income (loss) before extraordinary item $ 1.31 $ 1.34 $ 0.13 $ 0.20 $ 0.17 $ 0.09 $(0.09)

Extraordinary item, net of taxes ..... —(0.03) — ————

Net income (loss) ............. $1.31 $ 1.31 $ 0.13 $ 0.20 $ 0.17 $ 0.09 (0.09)

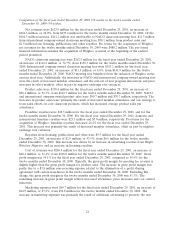

Items Affecting Comparability

Several events occurred during the fiscal years ended December 28, 2002 and December 29, 2001,

the eight months ended December 30, 2000, and the fiscal years ended April 29, 2000 and April 24,

1999 that affect the comparability of our financial statements. The nature of these events and their

impact on underlying business trends are as follows:

Acquisitions of North Jersey, San Diego and Eastern North Carolina. On January 18, 2002, we

acquired the franchise territory and certain business assets of our franchise in North Jersey for an

aggregate purchase price of $46.5 million. The acquisition was financed through additional borrowings

which were subsequently repaid by the end of the second quarter of 2002. On July 2, 2002 and

September 1, 2002, we acquired the assets of our franchises in San Diego and eastern North Carolina

for a total purchase price of $11.0 and $10.6 million, respectively. These acquisitions were financed

through cash from operations. All acquisitions were accounted for as purchases and accordingly, their

earnings have been included in our consolidated operating results since the dates of their acquisitions.

Reversal of Tax Valuation Allowance. During the fourth quarter of fiscal 2001, we reversed the

remaining tax valuation allowance set up in conjunction with the acquisition by Artal Luxembourg in

1999. At the time of the acquisition, we determined that it was more likely than not that a portion of

the deferred tax asset would not be utilized. Therefore, a valuation allowance of approximately

$72.1 million was established against the corresponding deferred tax asset. Based on our performance

since the acquisition, we have determined that the valuation allowance is no longer required.

Accordingly, the provision for taxes for the fiscal year ended December 29, 2001 included a one-time

reversal (credit) of the remaining balance of the valuation allowance of $71.9 million.

13