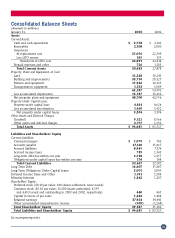

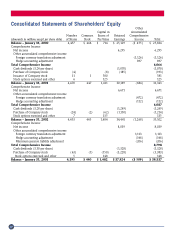

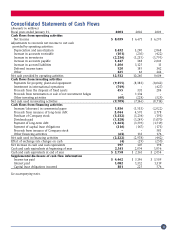

Walmart 2003 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2003 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

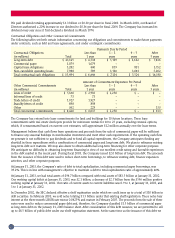

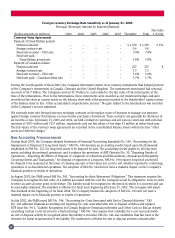

Foreign Currency Exchange Rate Sensitivity as of January 31, 2002

Principal (Notional) Amount by Expected Maturity Fair value

(Dollar amounts in millions) 2003 2004 2005 2006 2007 Thereafter Total 1/31/02

Currency Swap Agreements

Payment of Great Britain pounds

Notional amount – – – – – $ 1,250 $ 1,250 $ 192

Average contract rate – – – – – 0.6 0.6

Fixed rate received – USD rate – – – – – 7.4% 7.4%

Fixed rate paid –

Great Britain pound rate – – – – – 5.8% 5.8%

Payment of Canadian dollars

Notional amount – – – – – 325 325 8

Average contract rate – – – – – 1.5 1.5

Fixed rate received – USD rate – – – – – 5.6% 5.6%

Fixed rate paid – Canadian dollar rate – – – – – 5.7% 5.7%

During the fourth quarter of fiscal 2002, the Company terminated certain cross currency instruments that hedged portions

of the Company’s investments in Canada, Germany and the United Kingdom. The instruments terminated had notional

amounts of $6.7 billion. The Company received $1.1 billion in cash related to the fair value of the instruments at the

time of the terminations. Prior to the terminations, these instruments were classified as net investment hedges and were

recorded at fair value as current assets on the balance sheet with a like amount recorded in the shareholders’ equity section

of the balance sheet in line “other accumulated comprehensive income.” No gain related to the terminations was recorded

in the Company’s income statement.

We routinely enter into forward currency exchange contracts in the regular course of business to manage our exposure

against foreign currency fluctuations on cross-border purchases of inventory. These contracts are generally for durations of

six months or less. At January 31, 2003 and 2002, we held contracts to purchase and sell various currencies with notional

amounts of $185 million and $117 million, respectively, and net fair values of less than $1 million at either fiscal year.

The fair values of the currency swap agreements are recorded in the consolidated balance sheets within the line “other

assets and deferred charges.”

New Accounting Pronouncements

During fiscal 2003, the Company adopted Statement of Financial Accounting Standards No. 144, “Accounting for the

Impairment or Disposal of Long-Lived Assets.” FAS No. 144 develops an accounting model, based upon the framework

established in FAS No. 121, for long-lived assets to be disposed by sales. The accounting model applies to all long-lived

assets, including discontinued operations, and it replaces the provisions of ABP Opinion No. 30, “Reporting Results of

Operations – Reporting the Effects of Disposal of a Segment of a Business and Extraordinary, Unusual and Infrequently

Occurring Events and Transactions,” for disposal of segments of a business. FAS No. 144 requires long-lived assets held

for disposal to be measured at the lower of carrying amount or fair values less costs to sell, whether reported in continuing

operations or in discontinued operations. The adoption of FAS No. 144 did not have a material impact on the Company’s

financial position or results of operations.

In August 2001, the FASB issued FAS No. 143, “Accounting for Asset Retirement Obligations.” This statement requires the

Company to recognize the fair value of a liability associated with the cost the Company would be obligated to incur in order

to retire an asset at some point in the future. The liability would be recognized in the period in which it is incurred and can

be reasonably estimated. The standard is effective for fiscal years beginning after June 15, 2002. The Company will adopt

this standard at the beginning of its fiscal 2004. The Company believes the adoption of FAS No. 143 will not have a

material impact on its financial position or results of operations.

In July 2002, the FASB issued FAS No. 146, “Accounting for Costs Associated with Exit or Disposal Activities.” FAS

No. 146 addresses financial accounting and reporting for costs associated with exit or disposal activities and replaces

EITF Issue No. 94-3, “Liability Recognition for Certain Employee Termination Benefits and Other Costs to Exit an Activity

(including Certain Costs Incurred in a Restructuring).” FAS No. 146 requires that a liability for a cost associated with

an exit or disposal activity be recognized when the liability is incurred. FAS No. 146 also establishes that fair value is the

objective for initial measurement of the liability. The statement is effective for exit or disposal activities initiated after

28