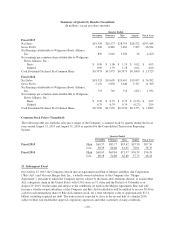

Walgreens 2015 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2015 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Report on Internal Control Over Financial Reporting

Management’s report on internal control over financial reporting and the report of Deloitte & Touche LLP, the

Company’s independent registered public accounting firm, related to their assessment of the effectiveness of

internal control over financial reporting are included in Part II, Item 8 of this Form 10-K and are incorporated in

this Item 9A by reference.

Changes in Internal Control over Financial Reporting

In connection with the evaluation pursuant to Exchange Act Rule 13a-15(d) of the Company’s internal control

over financial reporting (as defined in Exchange Act Rule 13a-15(f)) by the Company’s management, including

its CEO and CFO, except as noted below, no changes during the quarter ended August 31, 2015 were identified

that have materially affected, or are reasonably likely to materially affect, the Company’s internal control over

financial reporting. As a result of the closing of the Second Step Transaction, the Company has incorporated

internal controls over significant processes specific to the acquisition that it believes to be appropriate and

necessary in consideration of the level of related integration. As the post-closing integration continues, the

Company will continue to review the internal controls and processes of Alliance Boots and may take further steps

to integrate such controls and processes with those of the Company.

Inherent Limitations on Effectiveness of Controls

Our management, including the CEO and CFO, do not expect that our disclosure controls and procedures or our

internal control over financial reporting will prevent or detect all errors and all fraud. A control system, no matter

how well designed and operated, can provide only reasonable, not absolute, assurance that the control system’s

objectives will be met. The design of a control system must reflect the fact that there are resource constraints, and

the benefits of controls must be considered relative to their costs. Further, because of the inherent limitations in

all control systems, no evaluation of controls can provide absolute assurance that misstatements due to error or

fraud will not occur or that all control issues and instances of fraud, if any, within the Company have been

detected. These inherent limitations include the realities that judgments in decision-making can be faulty and that

breakdowns can occur because of simple error or mistake. Controls can also be circumvented by the individual

acts of some persons, by collusion of two or more people, or by management override of the controls. The design

of any system of controls is based in part on certain assumptions about the likelihood of future events, and there

can be no assurance that any design will succeed in achieving its stated goals under all potential future

conditions. Projections of any evaluation of controls effectiveness to future periods are subject to risks. Over

time, controls may become inadequate because of changes in conditions or deterioration in the degree of

compliance with policies or procedures.

Item 9B. Other Information

None.

- 124 -