US Cellular 2014 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2014 US Cellular annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

2 U.S. CELLULAR

choose from a competitive portfolio of the

products they want, including Samsung, Apple,

Motorola, and LG smartphones and connected

devices. Our attractive plans and pricing seal the

deal.

Also in 2014, we expanded our retail distribution

network. In addition to our own U.S. Cellular stores,

customers can purchase our plans and products

when they are at select Wal-Mart, Sam’s Club, and

Dollar General retail locations, as well as on

Amazon.com.

Driving Revenue Growth and Profi ts

The return to customer growth enabled us to

deliver improved revenue growth over the second

through new plans and smartphone and

connected device penetration, our average

revenue per account (ARPA) increased by 10% to

higher subsidies associated with selling more

4G LTE devices, including Apple products.

Under our Shared Connect plans, for which 47% of

postpaid customers are now signed up, we are

moving aggressively to monetize the explosive

growth in data usage. As we focus increasingly on

selling shared plans with larger data buckets, the

important. Smartphone customers were 60% of

postpaid customers at the end of 2014, and

smartphones represented 81% of total handsets

sold for the year. Connected devices were 7% of

total devices sold for the year, helping to drive

growth in data usage.

In 2014, we began to reap the

we initiated in prior years.

In 2014, we began to reap the In 2014, we began to reap the

we initiated in prior years. we initiated in prior years.

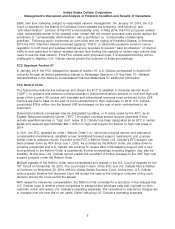

Smartphone Customers as a

Percentage of Postpaid Customers

Net Postpaid Additions (Losses)

(in thousands)

The strength of our

network is at the heart of

our value proposition.

The strength of our The strength of our

network is at the heart of network is at the heart of

our value proposition.our value proposition.

100

80

60

40

20

0

(20)

(40)

(60)

(80)

(100)

(71)

(93)

(26)

52

98

Q4 13 Q1 14 Q2 14 Q3 14 Q4 14

Q4 13 Q1 14 Q2 14 Q3 14 Q4 14

70%

60%

50%

40%

30%

20%

10%

0

51% 53% 55%

58%

4G

3G

60%