Starwood 2003 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2003 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

In addition, in early 2001, the Company wrote down its investments in various e-business ventures by

approximately $19 million based on the market conditions for the technology sector at the time and

management's assessment that the impairment of these investments was other-than-temporary. This special

charge was oÅset by the reversal of a $20 million restructuring charge taken in 1998 relating to a note

receivable, which previously had been written down due to non-performance.

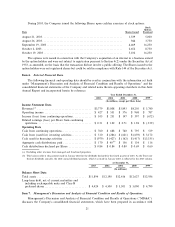

Depreciation and Amortization. Depreciation expense increased to $473 million in the year ended

December 31, 2002 compared to $430 million in the corresponding period of 2001. The increase was due to

additional depreciation resulting from capital expenditures at the Company's owned, leased and consolidated

joint venture hotels including the opening of the W Times Square in December 2001 and the Westin Dublin in

September 2001, as well as costs to reposition the W Lakeshore and the W Midland hotels in Chicago and

capital expenditures on technology development. Amortization expense decreased to $15 million in the year

ended December 31, 2002 compared to $88 million in the corresponding period of 2001. The decrease in the

amortization expense was primarily attributable to the implementation of SFAS No. 142, ""Goodwill and

Other Intangible Assets,'' which resulted in a $75 million pretax reduction in amortization expense.

Gain on Sale of VOI Notes Receivable. Gains from the sale of VOI receivables of $16 million and

$12 million in 2002 and 2001, respectively, are primarily due to the sale of $133 million and $226 million of

vacation ownership receivables during the years ended December 31, 2002 and 2001, respectively. Included in

the $226 million of VOI receivable sales in 2001 are $145 million of VOI receivables which were repurchased

from existing securitizations.

Net Interest Expense. Interest expense for the years ended December 31, 2002 and 2001, which is net of

interest income of $2 million and $11 million, and discontinued operations allocations of $15 million and

$13 million for 2002 and 2001, respectively, decreased to $323 million from $354 million. Excluding

$30 million and $9 million related to the early extinguishment of debt for 2002 and 2001, respectively, and an

$11 million reversal of accrued interest on tax liabilities that have now been settled in 2002, net interest

expense decreased $41 million from the comparable period of the prior year. This decrease was due primarily

to lower interest rates compared to 2001 lower debt balances and the impact of certain Ñnancing transactions

during the past two years. The Company's weighted average interest rate was 5.64% at December 31, 2002

versus 5.10% at December 31, 2001.

Gain (loss) on Asset Dispositions and Impairments, Net. During 2002, the Company sold its

investment in Interval International, for a gain of $6 million. This gain is oÅset primarily by a net loss of

$3 million on the disposition of two hotels. In 2001, due to the September 11 Attacks and the weakening of the

U.S. economy, the Company conducted a comprehensive review of the carrying value of certain assets for

potential impairment. As a result, the Company recorded a net charge relating primarily to the impairment of

certain investments totaling $57 million.

Income Tax Expense. The eÅective income tax rate for the year ended December 31, 2002 decreased to

0.7% compared to 21.7% in the corresponding period in 2001. The 2002 rate includes beneÑts related to

approximately $39 million of various adjustments to federal and state tax liabilities resulting from the

successful settlement of tax matters dating back to 1993. The Company's eÅective income tax rate is

determined by the level and composition of pretax income subject to varying foreign, state and local taxes and

other items. The tax rate for the year ended December 31, 2002 is signiÑcantly lower than the prior year due to

the combination of lower pretax income, the distribution of $0.84 per share and the cessation of amortization

of goodwill (as discussed above), which was not deductible for tax purposes.

Discontinued Operations

For the year's ended 2002 and 2001, loss from discontinued operations represents the results of the

Principe, net of $15 million and $13 million, of allocated interest expense, respectively. In June 2003, the

Company sold the Principe with no continuing involvement.

During 2002, the Company recorded an after tax gain of $109 million from discontinued operations

primarily related to the issuance of new Internal Revenue Service (""IRS'') regulations in early 2002, which

29