Sears 2008 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2008 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

SEARS HOLDINGS CORPORATION

Notes to Consolidated Financial Statements—(Continued)

Reorganization. Accordingly, the remaining 2.1 million of the 31.9 million shares set aside for distribution have been (or are

in the process of being) distributed to holders of Class 5 claims. The actual amount of allowed Class 5 claims was

approximately $4 billion, which is less than the $4.3 billion estimate provided for in the Plan of Reorganization.

Bankruptcy-Related Settlements

In fiscal 2008, fiscal 2007, and fiscal 2006, we recognized recoveries of $5 million, $18 million, and $14 million,

respectively, from vendors who had received cash payments for pre-petition obligations (“critical vendor claims”) or

preference payments. During fiscal 2008, the Company received 126,385 shares of common stock (weighted average price of

$94.61 per share) with an approximate value of $12 million from the Class 5 distribution referenced above. Of this amount

$5 million was recognized as a recovery gain in other income as they relate to recoveries from vendors who had received

cash payments for pre-petition obligations (critical vendor claims) or preference payments. The remaining $7 million was

recorded as capital in excess of par value as these shares are the result of a fiscal 2004 transaction in which the Company

entered into settlement agreements with past providers of surety bonds to resolve all issues in connection with their

pre-petition claims. In accordance with the terms of the settlement agreements, Kmart assumed responsibility for the future

obligations under the bonds issued with respect to the Predecessor Company’s workers’ compensation insurance program

and was assigned the Class 5 claims against the Company.

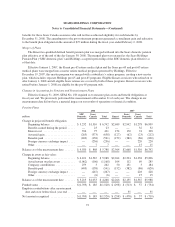

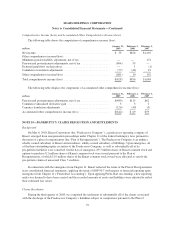

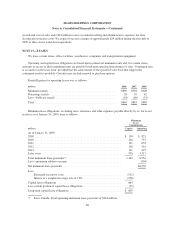

NOTE 11—INCOME TAXES

millions 2008 2007 2006

Income before income taxes

U.S. ........................................................................... $(407) $ 953 $2,125

Foreign ........................................................................ 591 499 346

Total ...................................................................... $ 184 $1,452 $2,471

Income tax expense

Current:

Federal .................................................................... $ (70) $ 76 $ 426

State and local .............................................................. 32 43 75

Foreign .................................................................... 199 98 80

Total .......................................................................... 161 217 581

Deferred:

Federal .................................................................... (60) 253 258

State and local .............................................................. (11) 2 44

Foreign .................................................................... (5) 78 50

(76) 333 352

Total .......................................................................... $ 85 $ 550 $ 933

2008 2007 2006

Effective tax rate reconciliation

Federal income tax rate ........................................................... 35.0% 35.0% 35.0%

State and local taxes net of federal tax benefit .......................................... 7.2 2.0 3.1

Tax credits ..................................................................... (6.3) (0.4) (0.3)

Resolution of income tax matters .................................................... (6.8) 0.5 (0.9)

Basis difference in domestic subsidiary ............................................... (30.2) 0.3 0.4

Canadian rate differential on minority interest ......................................... (2.3) — —

Nondeductible goodwill ........................................................... 50.0 — —

Other .......................................................................... (0.4) 0.5 0.5

46.2% 37.9% 37.8%

80