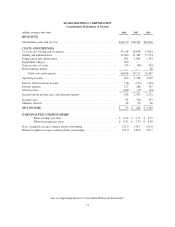

Sears 2008 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2008 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

SEARS HOLDINGS CORPORATION

Notes to Consolidated Financial Statements—(Continued)

inception and at least quarterly thereafter, whether the derivatives that are used in hedging transactions are highly

effective in offsetting changes in either the fair value or cash flows of the hedged item. If it is determined that a

derivative ceases to be a highly effective hedge, we discontinue hedge accounting.

For interest rate swaps and caps that have been designated and qualify as hedges, both the effective and

ineffective portions of the changes in the fair value of the derivative, along with the offsetting gain or loss on the

designated hedged item that is attributable to the hedged risk, are recognized in the consolidated statements of

income in the same account as the hedged item, as a component of interest expense. Changes in the fair value of

interest rate swaps and caps that do not qualify as hedges are recognized currently as a component of interest

expense. The foreign currency forward contracts are recorded on the consolidated balance sheet at fair value and,

to the extent they have been designated and qualify for hedge accounting treatment, an offsetting amount is

recorded as a component of other comprehensive income, net of income tax effects. Changes in the fair value of

those forward contracts for which hedge accounting is not applied are recorded in the consolidated statement of

income as a component of other income. Certain of our currency forward contracts require collateral to be posted

in the event our liability under such contracts reaches a predetermined threshold. Cash collateral posted under

these contracts is recorded as part of our restricted cash balance.

We have, from time to time, invested our surplus cash in various securities and financial instruments,

including total return swaps, which are derivative instruments designed to synthetically replicate the economic

return characteristics of one or more underlying marketable equity securities. Such investments may be highly

concentrated and involve substantial risks. Changes in the fair value of the total return swaps are recognized as a

component of interest and investment income in our consolidated statements of income as they occur. We had no

investments in total return swaps as of January 31, 2009 or February 2, 2008.

Fair Value of Financial Instruments

We adopted SFAS No. 157, “Fair Value Measurements” on February 3, 2008. SFAS No. 157 defines fair

value, establishes a framework for measuring fair value in GAAP and expands disclosure requirements about fair

value measurements. Under SFAS No. 157, fair value is considered to be the exchange price in an orderly

transaction between market participants to sell an asset or transfer a liability at the measurement date. The fair

value definition under SFAS No. 157 focuses on an exit price, which is the price that would be received by

Holdings to sell an asset or paid to transfer a liability versus an entry price, which would be the price paid to

acquire an asset or received to assume a liability. Although SFAS No. 157 does not require additional fair value

measurements, it applies to other accounting pronouncements that require or permit fair value measurements.

Financial instruments that potentially subject Holdings to concentration of credit risk consist principally of

temporary cash investments, accounts receivable and derivative financial instruments. We place our cash and

cash equivalents in investment-grade, short-term instruments with high quality financial institutions and, by

policy, limit the amount of credit exposure in any one financial instrument. We use high credit quality

counterparties to transact our derivative transactions.

We determine the fair value of financial assets and liabilities based on the fair value hierarchy prescribed by

SFAS No. 157, which prioritizes the inputs to valuation techniques used to measure fair value into three levels.

See Note 5 to the consolidated financial statements for further information regarding our derivative positions.

Cash and cash equivalents, accounts receivable, merchandise payables, credit facility borrowings and

accrued liabilities are reflected in the consolidated balance sheet at cost, which approximates fair value due to the

short-term nature of these instruments. The fair value of our debt is disclosed in Note 4 to the consolidated

financial statements.

59