Rosetta Stone 2010 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2010 Rosetta Stone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

|

|

Table of Contents

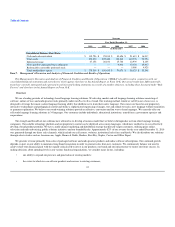

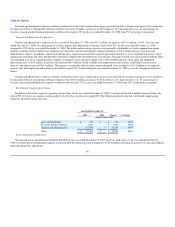

assets exceeds the future undiscounted net cash flows attributable to such assets. Impairment, if any, is recognized in the period of identification to the extent

the carrying amount of an asset exceeds the fair value of such asset. Based on our analysis, we believe that no impairment of our long-lived assets was

indicated as of December 31, 2010 and 2009.

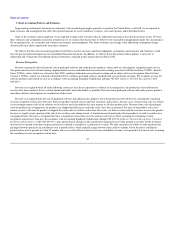

Income Taxes

For the years ended December 31, 2010, 2009 and 2008, we accounted for income taxes in accordance with Accounting Standards Codification topic

740, Income Taxes ("ASC 740"), which provides for an asset and liability approach to accounting for income taxes. Deferred tax assets and liabilities

represent the future tax consequences of the differences between the financial statement carrying amounts of assets and liabilities versus the tax bases of assets

and liabilities. Under this method, deferred tax assets are recognized for deductible temporary differences, and operating loss and tax credit carryforwards.

Deferred tax liabilities are recognized for taxable temporary differences. Deferred tax assets are reduced by a valuation allowance when, in the opinion of

management, it is more likely than not that some portion or all of the deferred tax assets will not be realized. The impact of tax rate changes on deferred tax

assets and liabilities is recognized in the year that the change is enacted.

In 2010, we recognized a tax benefit of $2.4 million due to the release of the valuation allowance on deferred tax assets which we believe are more likely

than not to be realized. Our effective income tax rate has benefited from the availability of previously unrealized deferred tax assets which we have utilized to

reduce tax expense for United Kingdom and Japanese income tax purposes. The release of our valuation allowance was determined in accordance with the

provisions of ASC 740, which requires an assessment of both positive and negative evidence when determining whether it is more likely than not that deferred

tax assets are recoverable; such assessment is required on a jurisdiction by jurisdiction basis. Historical operating income and continuing projected income

represent sufficient positive evidence that we have used to conclude that it is more likely than not that our deferred tax assets will be realized and accordingly,

a release of our valuation allowance was recorded in the fourth quarter of 2010.

In June 2006, the Financial Accounting Standards Board ("FASB") issued certain provisions in the Accounting Standards Codification topic 740-10-25,

Income Taxes: Overall: Recognition, ("ASC 740-10-25"), which clarify the accounting for uncertainty in income taxes recognized in an enterprise's financial

statements in accordance with ASC 740 and prescribe a recognition threshold and measurement attribute for the financial statement recognition and

measurement of a tax position taken or expected to be taken in a tax return. These provisions also provide guidance on de-recognition, classification, interest

and penalties, accounting in interim periods, disclosures, and transition. We adopted these recognition provisions of ASC 740-10-25 effective January 1,

2007. The adoption of ASC 740-10-25 did not have a material impact on our financial condition, results of operations or cash flows.

50