Oracle 2013 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2013 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

|

|

Table of Contents

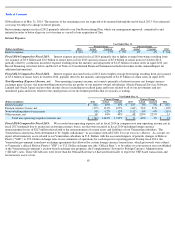

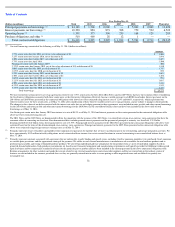

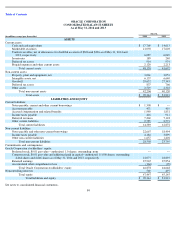

equivalents and marketable investments yielding an average 0.79% on a worldwide basis. The table below presents the approximate fair values

of our cash, cash equivalents and marketable securities and the related weighted average interest rates for our investment portfolio at May 31,

2014 and 2013.

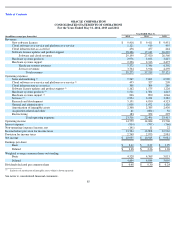

Interest Expense Risk

Our total borrowings were $24.2 billion as of May 31, 2014, consisting of $23.7 billion of fixed rate borrowings and $500 million of floating rate

borrowings. In July 2013, we issued €2.0 billion ($2.7 billion as of May 31, 2014) of fixed rate senior notes and $3.0 billion of senior notes

comprised of $500 million of floating rate notes and $2.5 billion of fixed rate notes as described in the “Recent Financing Activities” section of

Management’s Discussion and Analysis of Financial Condition and Results of Operations (Item 7) in this Annual Report.

In July 2013, we entered into certain interest rate swap agreements that have the economic effect of modifying the fixed interest obligations

associated with our $1.5 billion of 2.375% senior notes due January 2019 (2019 Notes) so that the interest payable on the 2019 Notes effectively

became variable based on LIBOR. In September 2009, we entered into certain interest rate swap agreements that have the economic effect of

modifying the fixed interest obligations associated with our $1.5 billion of 3.75% senior notes due July 2014 (2014 Notes) so that the interest

payable on the 2014 Notes effectively became variable based on LIBOR. The critical terms of the interest rate swap agreements and the 2019

Notes and 2014 Notes that the interest rate swap agreements pertain to match, including the notional amounts and maturity dates. We do not use

these interest rate swap arrangements or our fixed rate borrowings for trading purposes. We are accounting for these interest rate swap

agreements as fair value hedges pursuant to ASC 815, Derivatives and Hedging . Additional details regarding our senior notes and related

interest rate swap agreements are included in Note 8 and Note 11 of Notes to Consolidated Financial Statements, included elsewhere in this

Annual Report.

By entering into these interest rate swap arrangements, we have assumed risks associated with variable interest rates based upon LIBOR. As of

May 31, 2014, our 2014 Notes and 2019 Notes had effective interest rates of 1.29% and 0.88%, respectively, after considering the effects of the

aforementioned interest rate swap arrangements. Changes in the overall level of interest rates affect the interest expense that we recognize in our

statements of operations. An interest rate risk sensitivity analysis is used to measure interest rate risk by computing estimated changes in cash

flows as a result of assumed changes in market interest rates. As of May 31, 2014, if LIBOR-based interest rates increased by 100 basis points,

the change would increase our interest expense annually by approximately $22 million as it relates to our fixed to variable interest rate swap

agreements and floating rate borrowings.

Currency Risk

Foreign Currency Transaction and Translation Risks—Foreign Currency Borrowings and Related Hedges

In July 2013, we issued €1.25 billion of 2.25% notes due January 2021 (2021 Notes) and we entered into certain cross-currency swap

agreements to manage the related foreign exchange risk by effectively converting the fixed-rate Euro denominated debt, including the annual

interest payments and the payment of principal at maturity, to a fixed-rate, U.S. Dollar denominated debt. The economic effect of the swap

agreements was to eliminate the uncertainty of the cash flows in U.S. Dollars associated with the 2021 Notes by fixing the principal amount of

the 2021 Notes at $1.6 billion with an annual interest rate of 3.53%.

75

May 31,

2014

2013

(Dollars in millions)

Fair Value

Weighted

Average

Interest

Rate

Fair Value

Weighted

Average

Interest

Rate

Cash and cash equivalents

$

17,769

0.37%

$

14,613

0.50%

Marketable securities

21,050

1.14%

17,603

0.88%

Total cash, cash equivalents and marketable securities

$

38,819

0.79%

$

32,216

0.71%