MasterCard 2014 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2014 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

6

See Part I, Item 1A of this Report for a more detailed discussion of our legal and regulatory developments and risks.

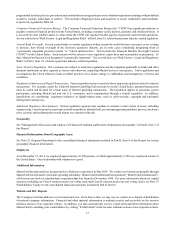

Our Business

Our Operations and Network

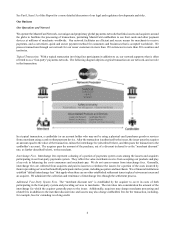

We operate the MasterCard Network, our unique and proprietary global payments network that links issuers and acquirers around

the globe to facilitate the processing of transactions, permitting MasterCard cardholders to use their cards and other payment

devices at millions of merchants worldwide. Our network facilitates an efficient and secure means for merchants to receive

payments, and a convenient, quick and secure payment method for consumers and businesses that is accepted worldwide. We

process transactions through our network for our issuer customers in more than 150 currencies in more than 210 countries and

territories.

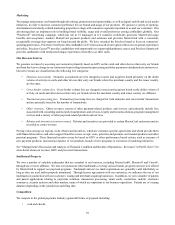

Typical Transaction. With a typical transaction involving four participants in addition to us, our network supports what is often

referred to as a “four-party” payments network. The following diagram depicts a typical transaction on our network, and our role

in that transaction:

In a typical transaction, a cardholder (or an account holder who may not be using a physical card) purchases goods or services

from a merchant using a card or other payment device. After the transaction is authorized by the issuer, the issuer pays the acquirer

an amount equal to the value of the transaction, minus the interchange fee (described below), and then posts the transaction to the

cardholder’s account. The acquirer pays the amount of the purchase, net of a discount (referred to as the “merchant discount”

rate, as further described below), to the merchant.

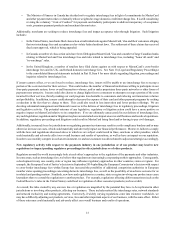

Interchange Fees. Interchange fees represent a sharing of a portion of payments system costs among the issuers and acquirers

participating in our four-party payments system. They reflect the value merchants receive from accepting our products and play

a key role in balancing the costs consumers and merchants pay. We do not earn revenues from interchange fees. Generally,

interchange fees are collected from acquirers and paid to issuers to reimburse the issuers for a portion of the costs incurred by

them in providing services that benefit all participants in the system, including acquirers and merchants. We or financial institutions

establish “default interchange fees” that apply when there are no other established settlement terms in place between an issuer and

an acquirer. We administer the collection and remittance of interchange fees through the settlement process.

Additional Four-Party System Fees. The “merchant discount rate” is established by the acquirer to cover its costs of both

participating in the four-party system and providing services to merchants. The rate takes into consideration the amount of the

interchange fee which the acquirer generally pays to the issuer. Additionally, acquirers may charge merchants processing and

related fees in addition to the merchant discount rate, and issuers may also charge cardholders fees for the transaction, including,

for example, fees for extending revolving credit.