MasterCard 2014 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2014 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

5

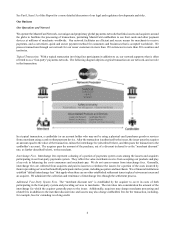

Strategic Partners. We work with merchants to help them enable new sales channels, create better purchase experiences, increase

revenues and fight fraud. We partner with large digital and mobile providers and telecommunication companies to support their

digital payment solutions with our technology, expertise and security protocols. We help national and local governments drive

increased financial inclusion and efficiency, reduce costs, increase transparency to reduce crime and corruption and advance social

programs. For consumers, we provide better, safer and more convenient ways to pay. We provide financial institutions with

solutions to help them increase revenue and increase preference for their MasterCard-branded products.

Recent Business and Legal/Regulatory Developments

Product Innovation. We have launched and extended products and platforms that take advantage of physical/digital convergence,

where consumers are increasingly seeking to use their cards to pay when, where and how they want. Among our recent

developments:

• In 2014, we expanded the availability of MasterPass™, our global digital platform. It provides an easy and secure way

to shop for all types of transactions (in-store, online and via mobile devices) by storing payment information in one

convenient and secure place and enabling payment with a click or touch.

• We are using our digital technologies and security protocols to develop mobile solutions to make shopping and selling

experiences simpler, faster, and safer for both consumers and merchants. One of the most prominent examples of this

in 2014 was the launch of Apple Pay™, which uses MasterCard Digital Enablement Service (MDES), the platform that

powers MasterPass and allows a connected device to be used as a safe and secure way to pay for everyday shopping.

Safety and Security. Our focus on security is embedded in our products, our systems and our network, as well as our analytics to

prevent fraud:

• We continue to lead the migration to EMV, the global standard for chip technology, to bring its fraud prevention benefits

to our U.S. customers, consumers and merchants.

• In the digital space, we are advancing the development of an industry-open standard for tokenization, which helps protect

sensitive cardholder information for digital transactions, significantly reducing fraud and delivering benefits to both

issuers and merchants.

• Among the products we launched in this area in 2014 is MasterCard SafetyNet™, which provides protection for issuers

from attacks that can disable their systems.

Financial Inclusion. We are focused on addressing financial inclusion, reaching people without access to an electronic account

that allows them to store and use money. In 2014, we worked with governments across several geographies to develop and roll

out electronic payments solutions and social payment distribution mechanisms.

Acquisitions and Investments. In 2014, we acquired eight new businesses focused on expanding our footprint and enhancing

critical capabilities, particularly around core processing activities, digital and mobile solutions and loyalty and rewards.

Legal and Regulatory. We operate in a dynamic and rapidly evolving legal and regulatory environment, with heightened regulatory

and legislative scrutiny and other legal challenges, particularly with respect to interchange fees (as discussed below under “Our

Operations and Network”). Recent developments include:

• European Union - In 2014, the European Commission’s proposed legislation relating to payment system regulation of

cards issued and acquired within the European Economic Area was amended by both the European Union Parliament

and the European Council of Ministers. Following discussions among all three governing institutions, the resulting

revised proposal includes, among other things, caps on consumer credit and debit interchange fees, “honor all cards”

rule restrictions, certain surcharging prohibitions, “co-badge” rule prohibitions and separation of brand and processing

in terms of accounting, organization and decision making. Final legislation is expected to be adopted during the first

half of 2015. We are managing the potential impact of this legislation on our business. See the risk factor in “Legal and

Regulatory Risks” in Part I, Item 1A of this Report related to payments system risks for a more detailed description of

the legislation and its potential impact.

• Russia - In response to the global sanctions imposed as a result of the Ukraine conflict, the Russian government has

amended its National Payments Systems laws to require all payment systems to process domestic transactions through

a government-owned payment switch, which will modestly increase our costs of doing business in Russia. This

requirement is expected to become effective in 2015. We are actively working to comply with the regulation and manage

the impact as we continue our business in Russia.