JetBlue Airlines 2010 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2010 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

|

|

Cash and Cash Equivalents: Our cash and cash equivalents include money market securities and trade

deposits which are readily convertible into cash with maturities of three months or less when purchased, both

of which are considered to be highly liquid and easily tradable. These securities are valued using inputs

observable in active markets for identical securities and are therefore classified as level 1 within our fair value

hierarchy.

We maintain cash and cash equivalents with various high quality financial institutions or in short-term

duration high quality debt securities. Investments in highly liquid debt securities are stated at fair value. The

majority of our receivables result from the sale of tickets to individuals, mostly through the use of major credit

cards. These receivables are short-term, generally being settled shortly after the sale. The carrying values of all

other financial instruments approximated their fair values at December 31, 2010 and 2009.

Available-for-sale investment securities: During 2009, we purchased asset backed securities, which

were considered variable rate demand notes with contractual maturities generally greater than ten years with

interest reset dates often every 30 days or less. Also included in our available-for-sale investment securities are

certificate of deposits placed through an account registry service, or CDARS, and commercial paper with

original maturities greater than 90 days but less than one year. The fair values of these investments are based

on observable market data. We did not record any significant gains or losses on these securities during the

twelve months ended December 31, 2010.

Auction rate securities: ARS are long-term debt securities for which interest rates reset regularly at pre-

determined intervals, typically 28 days, through an auction process. We held ARS, with a total par value of

$85 million as of December 31, 2009. Beginning in February 2008, all of the ARS then held by us

experienced failed auctions which resulted in our continuing to hold these securities beyond the initial auction

reset periods. With auctions continuing to fail through the end of 2008, we classified all of our ARS then held

as long term trading securities as of December 31, 2008, since maturities of underlying debt securities range

from 20 to 40 years. Our classification as trading securities is based on our intent to trade the securities when

market opportunities arise in order to increase our liquid investments due to the current economic uncertainty.

The estimated fair value of these securities beginning in 2008 no longer approximated par value and was

estimated through discounted cash flows, a level 3 input. Our discounted cash flow analysis considered, among

other things, the quality of the underlying collateral, the credit rating of the issuers, an estimate of when these

securities are either expected to have a successful auction or otherwise return to par value, the expected

interest income to be received over this period, and the estimated required rate of return for investors. Because

of the inherent subjectivity in valuing these securities, we also considered independent valuations obtained for

each of our ARS in estimating their fair values as of December 31, 2009.

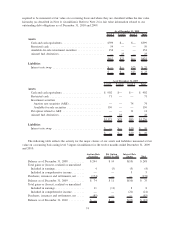

All of our ARS were collateralized by student loan portfolios (substantially all of which were guaranteed

by the United States Government), and had either a AAA or A rating. Despite the quality of the underlying

collateral, the market for ARS and other securities diminished due to the lack of liquidity experienced in the

market since early 2008 which continued for some time. Through September 30, 2008, we had experienced a

$13 million decline in fair value, which we had classified as temporary and reflected as an unrealized loss in

other comprehensive income. Through the fourth quarter of 2008, however, the lack of liquidity in the capital

markets not only continued, but deteriorated further, resulting in the decline in fair value totaling $67 million

at December 31, 2008. This decline in fair value was also deemed to be other than temporary due to the

continued auction failures and expected lack of liquidity in the capital markets continuing into the foreseeable

future, which resulted in a valuation loss being recorded in other income (expense). In February 2009, we sold

certain ARS for $29 million, an amount which approximated their fair value as of December 31, 2008. The

proceeds from these sales were used to reduce our $110 million line of credit then outstanding. In August

2009, we sold certain ARS for $25 million, an amount which approximated their fair value at that time. In

October 2009, we entered into an agreement with Citigroup Global Markets, Inc., under which they agreed to

purchase $158 million par value of the remaining ARS we held which were brokered by them. The

$120 million in cash proceeds from these sales did not result in significant gains or losses. In conjunction with

this transaction, we terminated the line of credit we had with Citigroup.

During 2008, following investigations by various regulatory agencies of the banks and broker-dealers that

sold ARS, UBS, one of the two broker-dealers from which we purchased ARS, subsequently reached a

75