JetBlue Airlines 2010 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2010 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

|

|

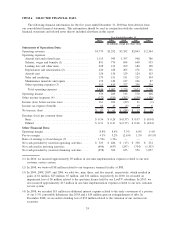

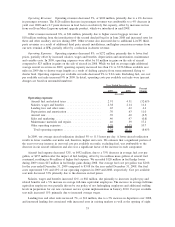

We maintain one of the lowest cost structures in the industry relative to the product we offer due to the

young average age of our fleet, a productive non-union workforce, and cost discipline. In 2011, we plan to

continue our focus on cost control while improving the JetBlue Experience for our customers. The largest

components of our operating expenses are aircraft fuel and related taxes and salaries, wages and benefits

provided to our crewmembers. Unlike most airlines, we have a policy of not furloughing crewmembers during

economic downturns, and a non-union workforce, which we believe provides us with more flexibility and

allows us to be more productive. The price and availability of aircraft fuel, which is our single largest

operating expense, are extremely volatile due to global economic and geopolitical factors that we can neither

control nor accurately predict. Sales and marketing expenses include advertising, fees paid to credit card

companies, and commissions paid for our participation in GDSs and OTAs. We believe our distribution costs

tend to be lower than those of most other airlines on a per unit basis because the majority of our customers

book directly through our website. Maintenance materials and repairs are expensed when incurred unless

covered by a third party services contract. Because the average age of our aircraft is 5.4 years, all of our

aircraft currently require less maintenance than they will in the future. Our maintenance costs will increase

significantly, both on an absolute basis and as a percentage of our unit costs, as our fleet ages. Other operating

expenses consist of purchased services (including expenses related to fueling, ground handling, skycap,

security and janitorial services), insurance, personnel expenses, cost of goods sold to other airlines by LiveTV,

professional fees, passenger refreshments, supplies, bad debts, communication costs, gains on aircraft sales and

taxes other than payroll and fuel taxes.

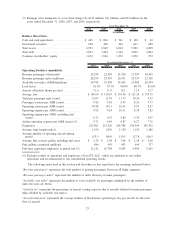

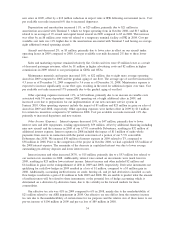

During 2010 fuel prices remained volatile, increasing 10% over average 2009 prices. We actively manage

our fuel hedge portfolio by entering into a variety of fuel hedge contracts in order to provide some protection

against volatility and further increases in fuel prices. In total, we effectively hedged 51% of our total 2010

fuel consumption. As of December 31, 2010, we had outstanding fuel hedge contracts covering approximately

37% of our forecasted consumption for the first quarter of 2011, 28% for the full year 2011, and 6% for the

full year 2012. We will continue to monitor fuel prices closely and intend to take advantage of fuel hedging

opportunities as they become available.

The airline industry is one of the most heavily taxed in the U.S., with taxes and fees accounting for

approximately 16% of the total fare charged to a customer. Airlines are obligated to fund all of these taxes

and fees regardless of their ability to pass these charges on to the customer. Additionally, if the TSA changes

the way the Aviation Security Infrastructure Fee is assessed, our security costs may be higher.

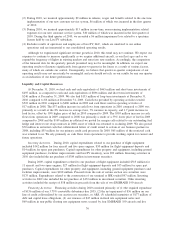

The airline industry has been intensely competitive in recent years, due in part to persistently high fuel

prices and the adverse financial condition of many of the domestic airlines, leading to significant

consolidation, bankruptcies and liquidation. In 2010, industry consolidation activities continued and further

impacted the competitive landscape, most notably with the merger of United Airlines and Continental Airlines,

which created the world’s largest airline and became effective in October 2010, on the heels of the Delta Air

Lines and Northwest Airlines merger in 2009. Additionally, in September 2010, low cost carrier Southwest

Airlines announced plans to acquire AirTran Airways.

We continue to focus on maintaining an adequate liquidity level. Our goal is to continue to be diligent

with our liquidity, thereby managing our capital expenditures to accommodate a sustainable growth plan. We

have manageable scheduled debt maturities in 2011 totaling approximately $185 million, which we believe

will enable us to achieve our liquidity goals.

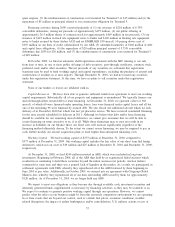

Our ability to be profitable in this competitive environment depends on, among other things, continuing

to provide high quality customer service, operating at costs equal to or lower than those of our competitors

and maintaining adequate liquidity levels. Although we have been able to raise capital and continue to grow in

recent years, the highly competitive nature of the airline industry and the impact of economic conditions could

prevent us from attaining the passenger traffic or yields required to be profitable in new and existing markets.

The highest levels of traffic and revenue on our routes to and from Florida are generally realized from

October through April and on our routes to and from the western United States in the summer. Our VFR

markets continue to complement our leisure-driven markets from both a seasonal and day of week perspective.

Many of our areas of operations in the Northeast experience bad weather conditions in the winter, causing

increased costs associated with de-icing aircraft, cancelled flights and accommodating displaced customers.

29