Holiday Inn 2006 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2006 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

Operating and financial review

Business overview

Market and competitive environment

IHG operates in the global hotel market which has an estimated

total room capacity of 18.8 million rooms. Room capacity has been

growing at approximately 3% per annum over the last five years.

The hotel market is geographically concentrated with 12 countries

accounting for two-thirds of worldwide hotel room supply. The

Group has a leadership position (top three by room numbers)

in more of these markets than any other major hotel company.

The hotel market is, however, a fragmented market with the four

largest companies controlling only 11% of the global hotel room

supply and the 10 largest controlling less than 21%. The Group is

the largest of these companies by room numbers with a 3% market

share. The major competitors in this market include other large

global hotel companies, smaller hotel companies and independent

hotels.

Within the global market, a relatively low proportion of hotel rooms

are branded (see figure 1), but there has been an increasing trend

towards branded rooms. For example, Mintel, a market research

company, estimates that the proportion of branded rooms in

Europe has grown from 15% in 2000 to 25% in 2004. Larger

branded companies are therefore gaining market share at the

expense of smaller companies and independent hotels. IHG is

well positioned to benefit from this trend. Hotel owners are

increasingly recognising the benefits of working with a group such

as IHG which can offer a portfolio of brands to suit the different

real estate opportunities an owner may have. Furthermore, hotel

ownership is increasingly being separated from hotel operations,

encouraging hotel owners to use third parties such as IHG to

manage or franchise their hotels.

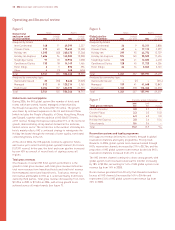

Figure 1

Percentage of branded hotel rooms by region 2004

North America 65%

South America 20%

Europe 25%

Middle East 25%

East Asia 25%

Source: Mintel (latest data available).

US market data indicates a steady increase in hotel industry

revenues, broadly in line with Gross Domestic Product, with growth

of approximately 1-1.5% per annum in real terms since 1967, driven

by a number of underlying trends:

• change in demographics – as the population ages and becomes

wealthier, increased leisure time and income encourages more

travel and hotel visits;

• increase in travel volumes as low cost airlines grow rapidly;

• globalisation of trade and tourism;

• increase in affluence and freedom to travel within the Chinese

middle class; and

• increase in the preference for branded hotels amongst

consumers.

Potential negative trends include increased terrorism,

environmental considerations and economic factors such as rising

oil prices. Currently, however, there are no indications that demand

is being significantly affected by these factors.

Supply growth in the industry is cyclical, averaging between zero

and 5% per annum historically. The Group’s profit is partly

protected from supply pressure due to its model of third party

ownership of hotels under IHG management and franchise

contracts.

Strategy

IHG owns, operates and franchises hotels, with its brands being

represented in nearly 100 countries and territories around the

world. The strategy is to become the preferred hotel company for

guests and owners by building the strongest operating system in

the industry, focused on the largest markets and segments where

scale really counts. During 2006, IHG initiated a number of research

projects, the results of which will strengthen the Group’s strategy

with respect to brand development, franchising operations and

growth opportunities.

The Group has four stated strategic priorities:

• brand performance – to operate a portfolio of brands attractive

to both owners and guests that have clear market positions in

relation to competitors;

• excellent hotel returns – to generate higher owner returns

through revenue delivery and improved operating efficiency;

• market scale and knowledge – to accelerate profitable growth in

the largest markets where the Group currently has scale; and

• aligned organisation – to create a more efficient organisation

with strong core capabilities.

6 IHG Annual report and financial statements 2006

This Operating and financial review (OFR) provides a commentary

on the performance of InterContinental Hotels Group PLC

(the Group or IHG) for the financial year ended 31 December 2006.