Holiday Inn 2006 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2006 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

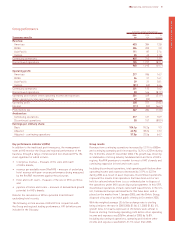

Central

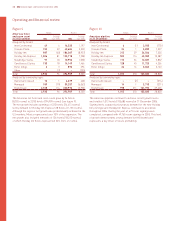

12 months ended 31 December

2006 2005 %

Central results £m £m change

Revenue 55 42 31.0

Gross central costs (136) (107) 27.1

Net central costs £m (81) (65) 24.6

Dollar equivalent $m (149) (118) 26.3

Net central costs increased by £16m to £81m and included

significant investment in new global research, designed to enable

higher quality brand development and enhance IHG’s franchising

capability; the increase also included higher IT infrastructure costs.

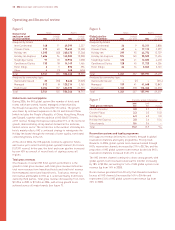

Corporate information

Other operating income and expenses

Other operating income and expenses of £27m includes the gain

on the sale of the Group’s investment in FelCor Lodging Trust, Inc.

Other operating income and expenses are treated as special items

by reason of their size or incidence and are excluded from the

calculation of adjusted earnings per share in order to provide a

more meaningful comparison of performance.

Net financing costs

Net financing costs decreased from £33m in 2005 to £11m in 2006,

primarily as a result of significantly lower average debt levels in the

year (£92m in 2006 compared with £700m in 2005). Financing costs

included £10m (2005 £5m) of interest costs associated with Priority

Club Rewards where interest is charged on the accumulated

balance of cash received in advance of the redemption points

awarded. The increase over 2005 arises from growth in the scheme

membership and higher interest rates. Financing costs in 2006 also

included £4m in respect of the InterContinental Boston finance

lease. Prior year costs included £9m in respect of the discontinued

Soft Drinks business.

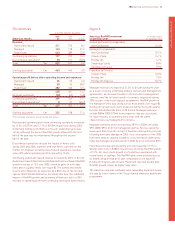

Taxation

The effective rate of tax on profit before tax, excluding the impact of

special items, was 24%. By also excluding the impact of prior year

items, which are included wholly within continuing operations, the

equivalent tax rate would be 36%. This rate is higher than the UK

statutory rate of 30% due mainly to overseas profits (predominantly

in the US) being subject to statutory rates higher than the UK

statutory rate, unrelieved losses and other disallowable expenses.

The equivalent effective rates for 2005 were 29% and 38%

respectively.

Taxation within special items totalled a credit of £94m (2005 £8m

credit). This represented, primarily, the release of provisions which

were special by reason of their size or incidence relating to tax

matters which were settled during the year, or in respect of which

the statutory limitation period had expired. In 2006, taxation special

items, in addition to such provision releases, included £12m for the

recognition of a deferred tax asset in respect of tax losses.

Net tax paid in 2006 totalled £49m (2005 £91m) including £6m

in respect of disposals.

Gain on disposal of assets

The gain on disposal of assets, net of related tax, totalled £117m

in 2006 and primarily comprised the gain on the sale of seven

InterContinental hotels to MSREF.

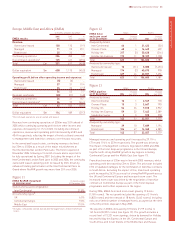

Earnings

Basic earnings per share in 2006 were 104.1p, compared with

95.2p in 2005. Adjusted earnings per share were 42.9p, against

38.2p in 2005. Adjusted continuing earnings per share were 37.5p,

66.7% up on last year.

Dividends

The Board has proposed a final dividend per share of 13.3p; with the

interim dividend of 5.1p, the normal dividend for 2006 will total 18.4p.

Share price and market capitalisation

The IHG share price closed at 1262.0p on 31 December 2006, up

from 839.5p on 31 December 2005. The market capitalisation of

the Group at the year end was £4.5bn.

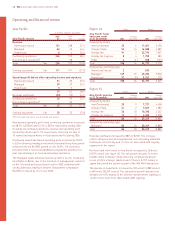

Cash flow

The net movement in cash and cash equivalents in the 12 months

to 31 December 2006 was an outflow of £152m. This included net

cash inflows from operating activities of £230m, net cash inflows

from investing activities of £620m and net cash outflows from

financing activities of £1,002m.

Proceeds from the disposal of hotels and other financial assets

totalled £744m.

Capital expenditure totalled £124m and included a major

refurbishment at the InterContinental London Park Lane and

the completion of a rooms refurbishment programme at the

InterContinental Hong Kong.

Cash outflows associated with shareholder returns during the year

included a special dividend of £497m and share buybacks of £260m.

Capital structure and liquidity management

Net debt at 31 December 2006 was £134m (see figure 16). In

November 2006, the InterContinental Boston opened; this hotel

is operated under a finance lease and the lease commitment of

£97m is therefore included within Group borrowings.

Gearing (net debt expressed as a percentage of IHG shareholders’

equity) at 31 December 2006 was 20%.

IHG Operating and financial review 15

Operating and financial review