Harley Davidson 2013 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2013 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

83

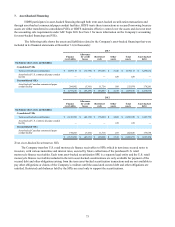

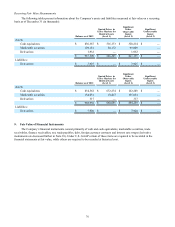

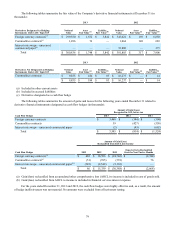

During 2013, the Company issued $650.0 million of secured notes through one term asset-backed securitization

transaction. During 2012, the Company issued $675.3 million of secured notes through one term asset-backed securitization

transaction. Additionally, during 2012, the Company issued $89.5 million of secured notes through the sale of notes that had

been previously retained as part of the December 2009, August 2011, and November 2011 term asset-backed securitization

transactions. These notes were sold at a premium, and at December 31, 2013 and 2012, the unaccreted premium associated with

these notes was $0.5 million and $1.2 million, respectively. Approximately $334.6 million and $399.5 million of the obligations

under the secured notes were classified as current at December 31, 2013 and 2012, respectively, based on the contractual

maturities of the restricted finance receivables. The term-asset backed securitization transactions are further discussed in Note

7.

No medium-term notes were issued in 2013. In January 2012, HDFS issued $400.0 million of medium-term notes which

mature in March 2017 and have an annual interest rate of 2.70%. In September 2012, HDFS issued $600.0 million of medium-

term notes which mature in September 2015 and have an annual interest rate of 1.15%. All of HDFS’ medium-term notes

(collectively, the Notes) provide for semi-annual interest payments and principal due at maturity. Unamortized discounts on the

Notes reduced the balance by $1.5 million and $2.2 million at December 31, 2013 and 2012, respectively.

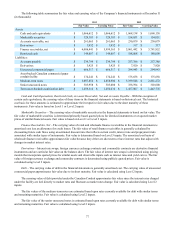

During 2013, 2012, and 2011, HDFS repurchased an aggregate of $23.0 million, $16.6 million, and $49.9 million

respectively, of its 6.80% medium-term notes which mature in June 2018. As a result, HDFS recognized in financial services

interest expense $4.9 million, $4.3 million, and $9.6 million of loss on extinguishment of debt, respectively, which included

unamortized discounts and fees. During December 2012, $400.0 million of the 5.25% medium-term notes matured, and the

principal and accrued interest were paid in full.

In February 2009, the Company issued $600.0 million of senior unsecured notes in an underwritten offering. The senior

unsecured notes provide for semi-annual interest payments and principal due at maturity. The senior unsecured notes mature in

February 2014 and have an annual interest rate of 15%. During the fourth quarter of 2010, the Company repurchased $297.0

million of the $600.0 million senior unsecured notes at a price of $380.8 million. As a result of the transaction, the Company

incurred a loss on debt extinguishment of $85.2 million which also included $1.4 million of capitalized debt issuance costs that

were written-off. The Company used cash on hand for the repurchase and the repurchased notes were canceled.

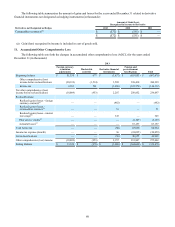

HDFS and the Company are subject to various operating and financial covenants related to the Global Credit Facilities

and various operating covenants under the Notes and the U.S. and Canadian asset-backed commercial paper conduit facilities.

The more significant covenants are described below.

The covenants limit the Company’s and HDFS’ ability to:

• incur certain additional indebtedness;

• assume or incur certain liens;

• participate in certain mergers, consolidations, liquidations or dissolutions; and

• purchase or hold margin stock.

Under the financial covenants of the Global Credit Facilities, the consolidated debt to equity ratio of HDFS cannot

exceed 10.0 to 1.0. In addition, the Company must maintain a minimum interest coverage ratio of at least 2.25 to 1.0 for each

fiscal quarter through June 2013 and at least 2.5 to 1.0 for each fiscal quarter thereafter. No financial covenants are required

under the Notes or the U.S. or Canadian asset-backed commercial paper conduit facilities.

At December 31, 2013 and 2012, HDFS and the Company remained in compliance with all of these covenants.