Harley Davidson 2013 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2013 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

60

Inventories – Inventories are valued at the lower of cost or market. Substantially all inventories located in the United

States are valued using the last-in, first-out (LIFO) method. Other inventories totaling $210.7 million at December 31, 2013

and $195.0 million at December 31, 2012 are valued at the lower of cost or market using the first-in, first-out (FIFO) method.

Property, Plant and Equipment – Property, plant and equipment is recorded at cost. Depreciation is determined on the

straight-line basis over the estimated useful lives of the assets. The following useful lives are used to depreciate the various

classes of property, plant and equipment: buildings – 30 years; building equipment and land improvements – 7 years;

machinery and equipment –3 to 10 years; furniture and fixtures –5 years; and software – 3 to 7 years. Accelerated methods of

depreciation are used for income tax purposes.

Goodwill – Goodwill represents the excess of acquisition cost over the fair value of the net assets purchased. Goodwill is

tested for impairment, based on financial data related to the reporting unit to which it has been assigned, at least annually or

whenever events or changes in circumstances indicate that the carrying value may not be recoverable. The impairment test

involves comparing the estimated fair value of the reporting unit associated with the goodwill to its carrying amount, including

goodwill. If the carrying amount of the reporting unit exceeds its fair value, goodwill must be adjusted to its implied fair value.

During 2013 and 2012, the Company tested its goodwill balances for impairment and no adjustments were recorded to goodwill

as a result of those reviews.

Long-lived Assets – The Company periodically evaluates the carrying value of long-lived assets to be held and used when

events and circumstances warrant such review. If the carrying value of a long-lived asset is considered impaired, a loss is

recognized based on the amount by which the carrying value exceeds the fair value of the long-lived asset for assets to be held

and used. The Company also reviews the useful life of its long-lived assets when events and circumstances indicate that the

actual useful life may be shorter than originally estimated. In the event that the actual useful life is deemed to be shorter than

the original useful life, depreciation is adjusted prospectively so that the remaining book value is depreciated over the revised

useful life.

Asset groups classified as held for sale are measured at the lower of carrying amount or fair value less cost to sell, and a

loss is recognized for any initial adjustment required to reduce the carrying amount to the fair value less cost to sell in the

period the held for sale criteria are met. The fair value less cost to sell must be assessed each reporting period the asset group

remains classified as held for sale. Gains or losses not previously recognized resulting from the sale of an asset group will be

recognized on the date of sale.

Product Warranty and Safety Recall Campaigns – The Company currently provides a standard two-year limited warranty

on all new motorcycles sold worldwide, except for Japan, where the Company provides a standard three-year limited warranty

on all new motorcycles sold. In addition, the Company started offering a one-year warranty for Parts & Accessories (P&A) in

2012. The warranty coverage for the retail customer generally begins when the product is sold to a retail customer. The

Company maintains reserves for future warranty claims which are based primarily on historical Company claim information.

Additionally, the Company has from time to time initiated certain voluntary safety recall campaigns. The Company reserves for

all estimated costs associated with safety recalls in the period that the safety recalls are announced.

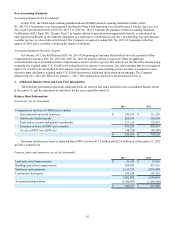

Changes in the Company’s warranty and safety recall liability were as follows (in thousands):

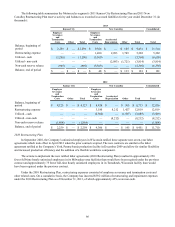

2013 2012 2011

Balance, beginning of period $ 60,263 $ 54,994 $ 54,134

Warranties issued during the period 59,022 54,394 44,092

Settlements made during the period (64,462)(67,247)(55,386)

Recalls and changes to pre-existing warranty liabilities 9,297 18,122 12,154

Balance, end of period $ 64,120 $ 60,263 $ 54,994

The liability for safety recall campaigns was $4.0 million, $4.6 million and $10.7 million at December 31, 2013, 2012

and 2011, respectively.

Derivative Financial Instruments – The Company is exposed to certain risks such as foreign currency exchange rate risk,

interest rate risk and commodity price risk. To reduce its exposure to such risks, the Company selectively uses derivative

financial instruments. All derivative transactions are authorized and executed pursuant to regularly reviewed policies and

procedures, which prohibit the use of financial instruments for speculative trading purposes.

All derivative instruments are recognized on the balance sheet at fair value (see Note 8). In accordance with ASC Topic

815, “Derivatives and Hedging,” the accounting for changes in the fair value of a derivative instrument depends on whether it

has been designated and qualifies as part of a hedging relationship and, further, on the type of hedging relationship. Changes in