Harley Davidson 2013 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2013 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

37

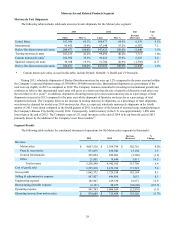

Other Matters

New Accounting Standards Not Yet Adopted

In July 2013, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU)

No. 2013-11 Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a

Tax Credit Carryforward Exists (ASU No. 2013-11). ASU No. 2013-11 amends the guidance within Accounting Standards

Codification (ASC) Topic 740, "Income Taxes", to require entities to present an unrecognized tax benefit, or a portion of an

unrecognized tax benefit in the financial statements as a reduction to a deferred tax asset for a net operating loss carryforward,

a similar tax loss, or a tax credit carryforward. The Company is required to adopt ASU No. 2013-11 beginning in the first

quarter of 2014 and is currently evaluating the impact of adoption.

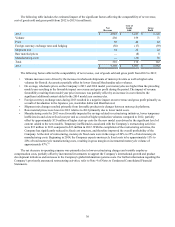

Critical Accounting Estimates

The Company’s financial statements are based on the selection and application of significant accounting policies, which

require management to make significant estimates and assumptions. Management believes that the following are some of the

more critical judgment areas in the application of accounting policies that currently affect the Company’s financial condition

and results of operations. Management has discussed the development and selection of these critical accounting estimates with

the Audit Committee of the Board of Directors.

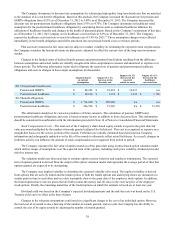

Allowance for Credit Losses on Finance Receivables – The allowance for uncollectible accounts is maintained at a level

management believes is adequate to cover the losses of principal in the existing finance receivables portfolio. HDFS performs a

periodic and systematic collective evaluation of the adequacy of the retail allowance. HDFS utilizes loss forecast models which

consider a variety of factors including, but not limited to, historical loss trends, origination or vintage analysis, known and

inherent risks in the portfolio, the value of the underlying collateral, recovery rates and current economic conditions including

items such as unemployment rates.

The wholesale portfolio is primarily composed of large balance, non-homogeneous finance receivables. HDFS’ wholesale

allowance evaluation is first based on a loan-by-loan review. A specific allowance is established for wholesale finance

receivables determined to be individually impaired when management concludes that the borrower will not be able to make full

payment of contractual amounts due based on the original terms of the loan agreement. The impairment is determined based on

the cash that the Company expects to receive discounted at the loan’s original interest rate or the fair value of the collateral, if

the loan is collateral-dependent. In establishing the allowance, management considers a number of factors including the

specific borrower’s financial performance as well as ability to repay. Finance receivables in the wholesale portfolio that are not

individually evaluated for impairment are segregated, based on similar risk characteristics, according to the Company’s internal

risk rating system and collectively evaluated for impairment. The related allowance is based on factors such as the Company’s

past loan loss experience, current economic conditions as well as the value of the underlying collateral.

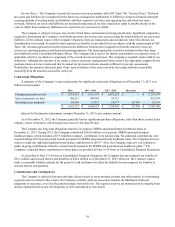

Product Warranty – Estimated warranty costs are reserved for motorcycles, motorcycle parts and motorcycle accessories

at the time of sale. The warranty reserve is based upon historical Company claim data used in combination with other known

factors that may affect future warranty claims. The Company updates its warranty estimates quarterly to ensure that the

warranty reserves are based on the most current information available.

The Company believes that past claim experience is indicative of future claims; however, the factors affecting actual

claims can be volatile. As a result, actual claims experience may differ from estimated which could lead to material changes in

the Company’s warranty provision and related reserves. The Company’s warranty liability is discussed further in Note 1 of

Notes to Consolidated Financial Statements.

Pensions and Other Postretirement Healthcare Benefits – The Company has a defined benefit pension plan and several

postretirement healthcare benefit plans, which cover employees of the Motorcycles segment. The Company also has unfunded

supplemental employee retirement plan agreements (SERPA) with certain employees which were instituted to replace benefits

lost under the Tax Revenue Reconciliation Act of 1993.

U.S. GAAP requires that companies recognize in their statement of financial position a liability for defined benefit

pension and postretirement plans that are underfunded or an asset for defined benefit pension and postretirement benefit plans

that are overfunded.

Pension, SERPA and postretirement healthcare obligations and costs are calculated through actuarial valuations. The

valuation of benefit obligations and net periodic benefit costs relies on key assumptions including discount rates, long-term

expected return on plan assets, future compensation and healthcare cost trend rates.