GE 2012 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2012 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

management’s discussion and analsis

68 GE 2012 ANNUAL REPORT

years, during which time relevant developments and new infor-

mation must be continuously evaluated to determine both the

likelihood of potential loss and whether it is possible to reasonably

estimate a range of possible loss. When a loss is probable but a

reasonable estimate cannot be made, disclosure is provided.

Disclosure also is provided when it is reasonably possible that

a loss will be incurred or when it is reasonably possible that the

amount of a loss will exceed the recorded provision. We regularly

review all contingencies to determine whether the likelihood of

loss has changed and to assess whether a reasonable estimate of

the loss or range of loss can be made. As discussed above, devel-

opment of a meaningful estimate of loss or a range of potential

loss is complex when the outcome is directly dependent on

negotiations with or decisions by third parties, such as regula-

tory agencies, the court system and other interested parties.

Such factors bear directly on whether it is possible to reasonably

estimate a range of potential loss and boundaries of high and

low estimates.

Further information is provided in Notes 2, 13 and 25.

Other Information

New Accounting Standards

In January 2013, the FASB issued amendments to existing stan-

dards for reporting comprehensive income. The amendments

expand disclosures about amounts that are reclassified out of

accumulated comprehensive income during the reporting period.

The amendments do not change existing recognition and mea-

surement requirements that determine net earnings and are

effective for our first quarter 2013 reporting.

In January 2013, the Emerging Issues Task Force reached a

final consensus that resolves conflicting guidance between ASC

Subtopics 810-10, Consolidation, and 830-30, Foreign Currency

Matters—Translation of Financial Statements, with regard to the

release of currency translation adjustments in certain circum-

stances. The Emerging Issues Task Force concluded that release

upon substantial liquidation applies to events occurring within a

foreign entity and that the loss of control model applies to events

related to investments in a foreign entity. The revised guidance

will apply prospectively to transactions or events occurring in fis-

cal years beginning after December 15, 2013.

In December 2011, the FASB issued amendments to existing

disclosure requirements for assets and liabilities that are offset

in the statement of financial position, which are effective for the

first quarter of 2013. In January 2013, the FASB clarified the scope

of the amendments to limit application of the disclosure require-

ments to derivatives, repurchase agreements, reverse purchase

agreements, securities borrowing and securities lending trans-

actions that are presented on a net basis in the statement of

financial position or are permitted to be netted under agree-

ments with counterparties. The amendments require expanded

disclosures about gross and net amounts of instruments that fall

within the scope of the amendment.

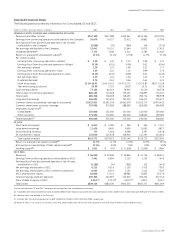

Research and Development

GE-funded research and development expenditures were

$4.5 billion, $4.6 billion and $3.9 billion in 2012, 2011 and 2010,

respectively. In addition, research and development funding from

customers, principally the U.S. government, totaled $0.7 billion,

$0.8 billion and $1.0 billion in 2012, 2011 and 2010, respectively.

Aviation accounts for the largest share of GE’s research and

development expenditures with funding from both GE and cus-

tomer funds. Power & Water and Healthcare also made significant

expenditures funded primarily by GE.

Orders and Backlog

GE infrastructure equipment orders increased 3% to $96.7 billion

at December 31, 2012. Total GE infrastructure backlog increased

4% to $209.5 billion at December 31, 2012, composed of equip-

ment backlog of $52.7 billion and services backlog of

$156.8 billion. Orders constituting backlog may be cancelled or

deferred by customers, subject in certain cases to penalties. See

the Segment Operations section for further information.