GE 2012 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2012 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

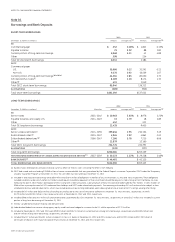

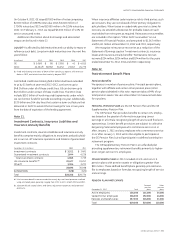

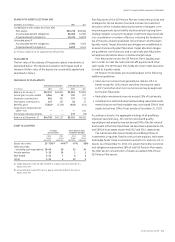

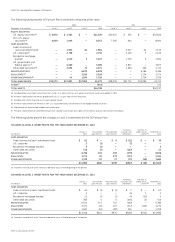

98 GE 2012 ANNUAL REPORT

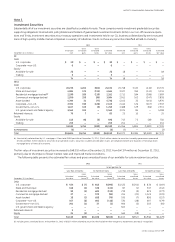

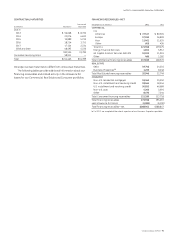

notes to consolidated financial statements

of potential comparables is often limited to publicly traded com-

panies where the characteristics of the comparative business

and ours can be significantly different, market data is usually not

available for divisions within larger conglomerates or non-public

subsidiaries that could otherwise qualify as comparable, and the

specific circumstances surrounding a market transaction (e.g.,

synergies between the parties, terms and conditions of the trans-

action, etc.) may be different or irrelevant with respect to our

business. It can also be difficult, under certain market conditions,

to identify orderly transactions between market participants in

similar businesses. We assess the valuation methodology based

upon the relevance and availability of the data at the time we per-

form the valuation and weight the methodologies appropriately.

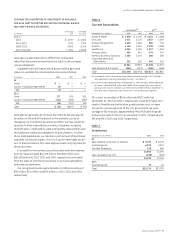

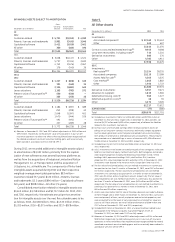

We performed our annual impairment test of goodwill for all

of our reporting units in the third quarter using data as of July 1,

2012. The impairment test consists of two steps: in step one, the

carrying value (including goodwill) of the reporting unit is com-

pared with its fair value, as if it were being acquired in a business

combination; in step two, which is applied when the carrying

value (including goodwill) of the reporting unit is more than its

fair value, the amount of goodwill impairment, if any, is derived

by deducting the fair value of the reporting unit’s assets and

liabilities from the fair value of its equity (net assets) as deter-

mined in step one to derive the implied fair value of goodwill, and

then comparing that implied amount with the carrying amount

of goodwill. In performing the valuations, we used cash flows

that reflected management’s forecasts and discount rates that

included risk adjustments consistent with the current market

conditions. Based on the results of our step one testing, the fair

values of each of the GE industrial reporting units and the CLL,

Consumer, Energy Financial Services and GECAS reporting units

exceeded their carrying values; therefore, the second step of the

impairment test was not required to be performed and no good-

will impairment was recognized.

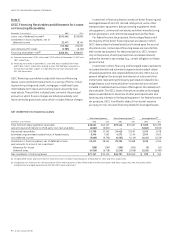

Our Real Estate reporting unit had a goodwill balance of

$926 million at December 31, 2012. As of July 1, 2012, the carry-

ing amount exceeded the estimated fair value of our Real Estate

reporting unit by approximately $1.8 billion. The estimated fair

value of the Real Estate reporting unit is based on a number of

assumptions about future business performance and investment,

including loss estimates for the existing finance receivable and

investment portfolio, new debt origination volume and margins,

and stabilization of the real estate market allowing for sales of

real estate investments at normalized margins. Our assumed dis-

count rate was 11% and was derived by applying a capital asset

pricing model and corroborated using equity analyst research

reports and implied cost of equity based on forecasted price to

earnings per share multiples for similar companies. Given the

volatility and uncertainty in the current commercial real estate

environment, there is uncertainty about a number of assump-

tions upon which the estimated fair value is based. Different loss

estimates for the existing portfolio, changes in the new debt

origination volume and margin assumptions, changes in the

expected pace of the commercial real estate market recovery,

or changes in the equity return expectation of market partici-

pants may result in changes in the estimated fair value of the Real

Estate reporting unit.

Based on the results of the step one testing, we performed

the second step of the impairment test described above as of

July 1, 2012. Based on the results of the second step analysis for

the Real Estate reporting unit, the estimated implied fair value

of goodwill exceeded the carrying value of goodwill by approxi-

mately $1.7 billion. Accordingly, no goodwill impairment was

required. In the second step, unrealized losses are reflected in

the fair values of an entity’s assets and have the effect of reduc-

ing or eliminating the potential goodwill impairment identified in

step one. The results of the second step analysis were attribut-

able to several factors. The primary drivers were the excess of

the carrying value over the estimated fair value of our Real Estate

Equity Investments, which approximated $2.6 billion at that time,

and the fair value premium on the Real Estate reporting unit

allocated debt. The results of the second step analysis are highly

sensitive to these measurements, as well as the key assumptions

used in determining the estimated fair value of the Real Estate

reporting unit.

Estimating the fair value of reporting units requires the use of

estimates and significant judgments that are based on a number

of factors including actual operating results. If current conditions

persist longer or deteriorate further than expected, it is reason-

ably possible that the judgments and estimates described above

could change in future periods.