Dollar General 2003 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2003 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

The Company has a $300 million revolving credit facility (the "Credit Facility"), which expires in June 2005. During 2004, the

Company intends to begin discussions with its lenders about amending or replacing the Credit Facility. As of January 30, 2004, the

Company had no outstanding borrowings and $22.5 million of standby letters of credit under the Credit Facility. The standby letters

of credit reduce the borrowing capacity of the Credit Facility. The Credit Facility contains certain financial covenants, all of which

the Company was in compliance with at January 30, 2004. See Note 5 to the Consolidated Financial Statements for further discus-

sion of the Credit Facility.

The Company has $200 million (principal amount) of 8 5/8% unsecured notes due June 15, 2010. This indebtedness was incurred

to assist in funding the Company’s growth. Interest on the notes is payable semi-annually on June 15 and December 15 of each year.

The note holders may elect to have these notes repaid on June 15, 2005, at 100% of the principal amount plus accrued and unpaid

interest. The Company may seek, from time to time, to retire its outstanding notes through cash purchases on the open market,

privately negotiated transactions or otherwise. Such repurchases, if any, will depend on prevailing market conditions, the

Company’s liquidity requirements, contractual restrictions and other factors. The amounts involved may be material.

Significant terms of the Company’s outstanding debt obligations could have an effect on the Company’s ability to incur additional

debt financing. The Credit Facility contains financial covenants which include the ratio of debt to EBITDAR (as defined in the debt

agreement), fixed charge coverage, asset coverage, minimum allowable consolidated net worth and maximum allowable capital

expenditures. The Credit Facility also places certain specified limitations on secured and unsecured debt. The Company’s out-

standing notes discussed above place certain specified limitations on secured debt and place certain limitations on the Company’s

ability to execute sale-leaseback transactions. The Company has generated significant cash flows from its operations during recent

years, and had no borrowings outstanding under the Credit Facility at any time during 2003. Therefore, the Company does not

believe that any existing limitations on its ability to incur additional indebtedness will have a material impact on its liquidity. Notes

5 and 7 to the Consolidated Financial Statements contain additional disclosures related to the Company’s debt and financing obli-

gations.

At January 30, 2004 and January 31, 2003, the Company had commercial letter of credit facilities totaling $218.0 million and $150.0

million, respectively, of which $111.7 million and $85.3 million, respectively, were outstanding for the funding of imported mer-

chandise purchases.

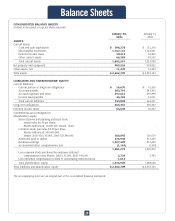

The Company believes that its existing cash balances ($398.3 million at January 30, 2004), cash flows from operations ($518.6 mil-

lion generated in 2003), the Credit Facility ($277.5 million available at January 30, 2004) and its anticipated ongoing access to the

capital markets, if necessary, will provide sufficient financing to meet the Company’s currently foreseeable liquidity and capital

resource needs.

Cash flows provided by operating activities. Cash flows from operations for 2003 compared to 2002 increased by $84.5 million. In

2002, the Company paid $162.0 million in settlement of the restatement-related class action lawsuit, as discussed in Note 7 to the

Consolidated Financial Statements, which did not recur in 2003. Partially offsetting this cash outflow were 2002 tax benefits total-

ing approximately $139.3 million, of which approximately $121 million either directly or indirectly related to the Company’s finan-

cial restatement and subsequent litigation settlement. The timing of these tax benefits was a significant component of the reduc-

tion of cash flows from deferred ($63.0 million) and current ($77.9 million) income taxes in 2003 compared to 2002. An increase

in accrued liabilities resulted in a $44.7 million increase in 2003 cash flows compared to 2002 due in part to the accrued SEC penal-

ty and increased 2003 bonuses described above, increased deferred compensation liabilities and increases in certain tax reserves.

Contributing to the increase in cash flows provided by operating activities in 2003 was an increase in net income of $36.1 million

driven by the improved operating results discussed above (see "Results of Operations").

Cash flows from operations for 2002 compared to 2001 increased by $168.4 million due principally to the increase in net income

described above and improved inventory productivity. As a result of the improvement in inventory turns to 3.8 times in 2002 from

3.5 times in 2001, the change in inventory in 2002 was an $8.0 million source of cash as compared against a $118.8 million use of

cash in 2001. Also affecting cash flows from operating activities was the restatement-related class action lawsuit settlement and

related tax effects described above.

Cash flows used in investing activities. The Company’s purchases of property and equipment in 2003 included the following: $63.2

million for new, relocated and remodeled stores; $22.0 million for systems-related capital projects; and $25.2 million for distribu-

tion and transportation-related capital expenditures. During 2003, the Company opened 673 new stores and relocated or remod-

eled 76 stores. Systems-related projects in 2003 included $5.9 million for point-of-sale and satellite technology and $3.1 million

related to debit/credit/EBT technology. Distribution and transportation expenditures in 2003 include $19.1 million at the Ardmore,

Oklahoma and South Boston, Virginia DCs primarily related to the ongoing expansion of those facilities.

M D & A

16