DIRECTV 2002 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2002 DIRECTV annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

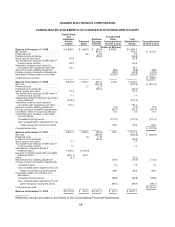

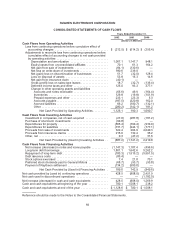

HUGHES ELECTRONICS CORPORATION

stock-based compensation for all stock-based compensation granted after December 31, 2002 in

accordance with the original transition provisions of SFAS No. 123. Adoption of this standard will result

in an increase in compensation cost recognized in operating results. Had Hughes followed the fair

value based method of accounting for stock-based compensation under SFAS No. 123 for the years

ended December 31, 2002, 2001 and 2000, pro forma earnings (loss) used for computation of

available separate consolidated net income (loss) would have been $(1,112.4) million, $(946.5) million

and $585.3 million, respectively.

In November 2002, the EITF reached a consensus on Issue No. 00-21, “Accounting for Revenue

Arrangements with Multiple Deliverables.” EITF Issue No. 00-21 addresses determination of whether

an arrangement involving more than one deliverable contains more than one unit of accounting and

how the related revenues should be measured and allocated to the separate units of accounting. EITF

Issue No. 00-21 will apply to revenue arrangements entered into after June 30, 2003; however, upon

adoption, the EITF allows the guidance to be applied on a retroactive basis, with the change, if any,

reported as a cumulative effect of accounting change in the consolidated statements of operations.

Hughes has not yet determined the impact this issue will have on its consolidated results of operations

or financial position, if any.

In June 2002, the FASB issued SFAS No. 146, “Accounting for Costs Associated with Exit or

Disposal Activities.” SFAS No. 146 generally requires the recognition of costs associated with exit or

disposal activities when incurred rather than at the date of a commitment to an exit or disposal plan.

SFAS No. 146 replaces previous accounting guidance provided by EITF Issue No. 94-3, “Liability

Recognition for Certain Employee Termination Benefits and Other Costs to Exit an Activity (including

Certain Costs Incurred in a Restructuring).” Hughes is required to implement SFAS No. 146 on

January 1, 2003. Hughes’ adoption of this standard on January 1, 2003 is not expected to have a

significant impact on Hughes’ consolidated results of operations or financial position.

In April 2002, the FASB issued SFAS No. 145, “Rescission of FASB Statements No. 4, 44 and 64,

Amendment of FASB Statement No. 13 and Technical Corrections.” SFAS No. 145 eliminates the

requirement to present gains and losses on the early extinguishment of debt as an extraordinary item,

and resolves accounting inconsistencies for certain lease modifications. Hughes’ adoption of this

standard on January 1, 2003 is not expected to have an impact on Hughes’ consolidated results of

operations or financial position.

Security Ratings

Debt ratings by the various rating agencies reflect each agency’s opinion of the ability of issuers to

repay debt obligations as they come due. Ratings below Baa3 and BBB- denote sub-investment grade

status for Moody’s and S&P, respectively. Ratings in the Ba/BB range generally indicate moderate

protection of interest and principal payments, potentially outweighed by exposure to uncertainties or

adverse conditions. Ratings in the B range generally indicate that the obligor currently has financial

capacity to meet its financial commitments but there is limited assurance over any long period of time

that interest and principal payments will be made or that other terms will be maintained. In general,

lower ratings result in higher borrowing costs. A security rating is not a recommendation to buy, sell, or

hold securities and may be subject to revision or withdrawal at any time by the assigning rating

organization.

Hughes

On December 11, 2002, Moody’s Investor Services (“Moody’s”) confirmed Hughes’ Ba3 senior

secured and senior implied rating. The rating outlook, which previously remained on review for possible

60