DIRECTV 2002 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2002 DIRECTV annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

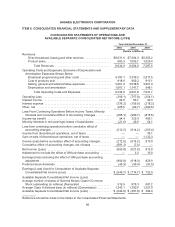

HUGHES ELECTRONICS CORPORATION

Equity Method Investments. Hughes holds 19.5% and 40.0% equity interests in LOC’s that are

the exclusive distributors of DIRECTV in Venezuela and Puerto Rico, respectively. During 2001,

Hughes began recording approximately 75.0% of the net losses incurred from these entities due to the

accumulation of net losses in excess of the other investors’ investments, and Hughes’ continued

funding of those businesses. During the years ended December 31, 2002, 2001 and 2000, DLA

recognized revenues of $189.9 million, $160.6 million, and $90.1 million, respectively, primarily for

sales of programming to the LOC’s. Broadcast programming and other costs associated with these

revenues were $110.4 million, $90.7 million, and $51.6 million during the years ended December 31,

2002, 2001 and 2000, respectively. Also during the years ended December 31, 2002, 2001 and 2000,

Hughes recognized equity method losses in “Other, net” of $54.1 million, $16.2 million, and $18.8

million, respectively. DLA had accounts receivable of $310.9 million and $217.5 million from the LOC’s

as of December 31, 2002 and 2001, respectively.

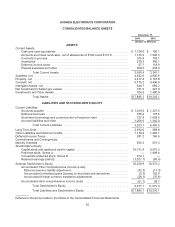

Accounting Changes

Hughes adopted SFAS No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets”

on January 1, 2002. SFAS No. 144 refined existing impairment accounting guidance and extended the

use of this accounting to discontinued operations. SFAS No. 144 allowed the use of discontinued

operations accounting treatment for both reporting segments and distinguishable components thereof.

SFAS No. 144 also eliminated the existing exception to consolidation of a subsidiary for which control

is likely to be temporary. The adoption of SFAS No. 144 did not have any impact on Hughes’

consolidated results of operations or financial position. However, operating results of discontinued

businesses such as DIRECTV Broadband, which previously would not have been reported as a

discontinued operation, will be reported as a discontinued operation under this new standard in future

periods.

Hughes also adopted SFAS No. 142, “Goodwill and Other Intangible Assets” on January 1, 2002.

SFAS No. 142 required that existing and future goodwill and intangible assets with indefinite lives not

be amortized, but written-down, as needed, based upon an impairment analysis that must occur at

least annually, or sooner if an event occurs or circumstances change that would more likely than not

result in an impairment loss. All other intangible assets are amortized over their estimated useful lives.

SFAS No. 142 required that Hughes perform step one of a two-part transitional impairment test to

compare the fair value of each reportable unit with its respective carrying amount, including goodwill. If

the carrying value exceeds the fair value, step two of the transitional impairment test must be

performed to measure the amount of the impairment loss, if any. SFAS No. 142 also required that

intangible assets be reviewed as of the date of adoption to determine if they continue to qualify as

intangible assets under the criteria established under SFAS No. 141, “Business Combinations,” and to

the extent previously recorded intangible assets do not meet the criteria that they be reclassified to

goodwill.

As part of Hughes’ acquisition of PRIMESTAR in 1999, dealer network and subscriber base

intangible assets were identified and valued in accordance with Accounting Principles Board (“APB”)

Opinion No. 16, “Business Combinations.” The dealer network intangible asset originally valued as part

of Hughes’ acquisition of PRIMESTAR was based on established distribution, customer service and

marketing capability that had been put in place by PRIMESTAR. The subscriber base intangible asset

originally valued as part of Hughes’ acquisition of PRIMESTAR was primarily based on the expected

non-contractual future cash flows to be earned over the life of the PRIMESTAR subscribers converted

to the DIRECTV service. In accordance with SFAS No. 142, Hughes completed a review of its

intangible assets and determined that the previously recorded dealer network and subscriber base

intangible assets established under APB Opinion No. 16 did not meet the contractual or other legal

57