Comcast 2007 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2007 Comcast annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

The deployment of digital subscriber line (“DSL”) technology allows

Internet access to be provided to subscribers over telephone lines

at data transmission speeds substantially greater than those of

dial-up modems. ILECs and other companies offer DSL service,

and several of them have increased transmission speeds, lowered

prices or created bundled service packages. In addition, some

ILECs, such as AT&T and Verizon, have built and are continuing to

build fiber-optic-based networks that allow them to provide data

transmission speeds that exceed those that can be provided with

DSL technology and are now offering these higher speed services

in many of our markets. The FCC has reduced the obligations of

ILECs to offer their broadband facilities on a wholesale or retail

basis to competitors, and it has freed their DSL services of com-

mon carrier regulation.

Various wireless phone companies are offering wireless high-speed

Internet services. In addition, in a growing number of commercial

areas, such as retail malls, restaurants and airports, wireless Wi-Fi

and WiMAX Internet service is available. Numerous local govern-

ments are also considering or actively pursuing publicly subsidized

Wi-Fi and WiMAX Internet access networks.

A number of cable operators have reached agreements to provide

unaffiliated ISPs access to their cable systems in the absence of

regulatory requirements. We reached access agreements with

several national and regional third-party ISPs, although to date

these ISPs have made limited use of their rights. We cannot pro-

vide any assurance, however, that regulatory authorities will not

impose so-called “open access” or similar requirements on us

as part of an industry-wide requirement. Additionally, Congress

and the FCC are considering creating certain rights for Internet

content providers and for users of high-speed Internet services by

imposing “net neutrality” requirements on service providers. These

requirements could adversely affect our high-speed Internet busi-

ness (see “Legislation and Regulation” below).

We expect competition for high-speed Internet service subscribers

to remain intense, with companies competing on service availability,

price, product features, customer service, transmission speeds and

bundled services.

Phone Services

Our digital phone service and our circuit-switched local phone

service compete against ILECs, wireless phone service providers,

competitive local exchange carriers (“CLECs”) and other VoIP serv-

ice providers. The ILECs have substantial capital and other

resources, longstanding customer relationships, and extensive

existing facilities and network rights-of-way. A few CLECs also

have existing local networks and significant financial resources.

We anticipate that by the end of 2008, approximately 91% of our

homes passed will have access to our digital phone service. We

expect some of our circuit-switched phone subscribers to migrate

to our digital phone service as we phase out our circuit-switched

phone service in 2008. The competitive nature of the phone busi-

ness may negatively affect demand for and pricing of our phone

services.

Advertising

We compete against a wide variety of media for the sale of adver-

tising, including local television broadcast stations, national tele-

vision broadcast networks, national and regional cable television

networks, local radio broadcast stations, local and regional news-

papers, magazines and Internet sites.

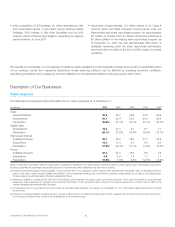

Programming Segment

The table below presents a summary of our most significant consolidated national programming networks as of December 31, 2007:

Programming Network

Approximate

U.S. Subscribers

(in millions) Description

E! 82 Pop culture and entertainment-related programming

The Golf Channel 67 Golf and golf-related programming

VERSUS 64 Sports and leisure programming

G4 55 Gamer lifestyle programming

Style 48 Lifestyle-related programming

Revenue for our programming networks is primarily generated from the sale of advertising and from monthly per subscriber license fees

paid by MVPDs that have typically entered into multiyear contracts to distribute our programming networks. To obtain long-term contracts

with distributors, we may make cash payments, provide an initial period in which license fee payments are waived or do both. Our pro-

gramming networks assist distributors with ongoing marketing and promotional activities to retain existing subscribers and acquire new

subscribers. Although we believe prospects of continued carriage and marketing of our programming networks by larger distributors are

generally good, the loss of one or more of such distributors could have a material adverse effect on our programming networks.

7Comcast 2007 Annual Report on Form 10-K