Comcast 2007 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2007 Comcast annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

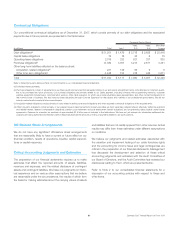

|

|

We use the notional amounts on the instruments to calculate

the interest to be paid or received. The notional amounts do

not represent the amount of our exposure to credit loss. The esti-

mated fair value approximates the payments necessary or proceeds

to be received to settle the outstanding contracts. We estimate inter-

est rates on variable debt and swaps using the average implied

forward London Interbank Offered Rate (“LIBOR”) for the year of

maturity based on the yield curve in effect on December 31, 2007,

plus the applicable margin in effect on December 31, 2007.

As a matter of practice, we typically do not structure our financial

contracts to include credit-ratings-based triggers that could affect

our liquidity. In the ordinary course of business, some of our

swaps could be subject to termination provisions if we do not

maintain investment grade credit ratings. As of December 31,

2007 and 2006, the estimated fair value of those swaps was a

liability of $3 million and $60 million, respectively. The amount to

be paid or received upon termination, if any, would be based on

the fair value of the outstanding contracts at that time.

Equity Price Risk Management

We are exposed to the market risk of changes in the equity prices

of our investments in marketable securities. We enter into various

derivative transactions in accordance with our policies to manage

the volatility relating to these exposures.

Through market value and sensitivity analyses, we monitor our

equity price risk exposures to ensure that the instruments are

matched with the underlying assets or liabilities, reduce our risks

relating to equity prices and maintain a high correlation to the risk

inherent in the hedged item.

To limit our exposure to and benefits from price fluctuations in the

common stock of some of our investments, we use equity deriva-

tive financial instruments. These derivative financial instruments,

which are accounted for at fair value, include equity collar agree-

ments, prepaid forward sales agreements and indexed or ex-

changeable debt instruments.

Except as described above in “Investment Income (Loss), Net,” the

changes in the fair value of the investments that we accounted for

as trading securities were substantially offset by the changes in the

fair values of the equity derivative financial instruments.

Refer to Note 2 to our consolidated financial statements for a dis-

cussion of our accounting policies for derivative financial instru-

ments and to Note 6 and Note 8 to our consolidated financial

statements for discussions of our derivative financial instruments.

35 Comcast 2007 Annual Report on Form 10-K