Capital One 1999 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 1999 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

54

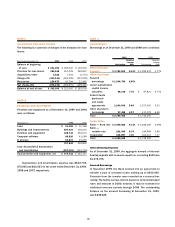

Premises and Equipment

Premises and equipment are stated at cost less accumulated

depreciation and amortization. Depreciation and amortization

expense are computed generally by the straight-line method

over the estimated useful lives of the assets. Useful lives for

premises and equipment are as follows: buildings and

improvements — 5–39 years; furniture and equipment — 3–10

years; computers and software — 3 years.

Marketing

The Company expenses marketing costs as incurred.

Credit Card Fraud Losses

The Company experiences fraud losses from the unauthorized

use of credit cards. Transactions suspected of being fraudulent

are charged to non-interest expense after a sixty-day investiga-

tion period.

Income Taxes

Deferred tax assets and liabilities are determined based on dif-

ferences between the financial reporting and tax bases of assets

and liabilities, and are measured using the enacted tax rates

and laws that will be in effect when the differences are expected

to reverse.

Comprehensive Income

As of December 31, 1999, cumulative other comprehensive

income, net of tax, consisted of $32,608 in net unrealized losses

on securities and $1,346 in foreign currency translation adjust-

ments. As of December 31, 1998 and 1997, cumulative other

comprehensive income, net of tax, consisted of $63,260 and

$2,612 in net unrealized gains on securities and $(2,605) and

$(73) in foreign currency translation adjustments, respectively.

As of December 31, 1999, substantially all of the net unrealized

loss on securities was comprised of gross unrealized losses.

Segments

The Company maintains three distinct business segments: lend-

ing, telecommunications and “other.” The lending segment is

comprised primarily of credit card lending activities. The telecom-

munications segment consists primarily of direct marketing

wireless service. “Other” consists of various non-lending new busi-

ness initiatives, none of which exceed the quantitative thresholds

for reportable segments in Statement of Financial Accounting

Standards (“SFAS”) No. 131, “Disclosures about Segments of

an Enterprise and Related Information” (“SFAS 131”).

The accounting policies of these reportable segments are

the same as those described above. Management measures the

performance of its business segments on a managed basis and

makes resource allocation decisions based upon several fac-

tors, including income before taxes, less indirect expenses.

Lending is the Company’s only reportable business segment,

based on the definitions provided in SFAS 131. Substantially all

of the Company’s reported assets, revenues and income are

derived from the lending segment in all periods presented.

All revenue is generated from external customers and is

predominantly derived in the United States. Revenues and oper-

ating losses from international operations comprised less than

6% and 7% of total managed revenues and operating income,

respectively, for the year ended December 31, 1999.

Recent Accounting Pronouncements

In June 1999, the FASB issued SFAS No. 137, “Accounting for

Derivative Instruments and Hedging Activities — Deferral of the

Effective Date of FASB Statement No. 133” (“SFAS 137”), which

defers the effective date of SFAS No. 133, “Accounting for Deriv-

ative Instruments and Hedging Activities” (together “SFAS 133

as amended”) to all fiscal quarters of all fiscal years beginning

after June 15, 2000. SFAS 133 as amended will require the

Company to recognize all derivatives on the balance sheet at

fair value. Derivatives that are not hedges must be adjusted to

fair value through earnings. If the derivative is a hedge, depend-

ing on the nature of the hedge, changes in the fair value of

derivatives will either be offset against the change in fair value

of the hedged assets, liabilities or firm commitments through

earnings or recognized in other comprehensive income until the

hedged item is recognized in earnings. The ineffective portion of

a derivative’s change in fair value will be immediately recog-

nized in earnings. The adoption of SFAS 133 as amended is not

expected to have a material effect on the results of the Com-

pany’s operations.