Capital One 1999 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 1999 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

30

The Company retains an interest in the trusts (“seller’s in-

terest”) equal to the amount of the receivables transferred to

the trust in excess of the principal balance of the certificates.

The Company’s interest in the trusts varies as the amount of the

excess receivables in the trusts fluctuates as the accounthold-

ers make principal payments and incur new charges on the se-

lected accounts. The securitization generally results in the

removal of the receivables, other than the seller’s interest, from

the Company’s balance sheet for financial and regulatory ac-

counting purposes.

The Company’s relationship with its customers is not

affected by the securitization. The Company acts as a servicing

agent and receives a fee.

Collections received from securitized receivables are used

to pay interest to certificateholders, servicing and other fees,

and are available to absorb the investors’ share of credit losses.

Amounts collected in excess of that needed to pay the above

amounts are remitted to the Company, as described in Servic-

ing and Securitizations Income.

Certificateholders in the Company’s securitization program

are generally entitled to receive principal payments either

through monthly payments during an amortization period or in

one lump sum after an accumulation period. Amortization may

begin sooner in certain circumstances, including if the annual-

ized portfolio yield (consisting, generally, of interest and fees)

for a three-month period drops below the sum of the certificate

rate payable to investors, loan servicing fees and net credit

losses during the period.

Prior to the commencement of the amortization or accu-

mulation period, all principal payments received on the trusts’

receivables are reinvested in new re-

ceivables to maintain the principal

balance of certificates. During the

amortization period, the investors’

share of principal payments is paid

to the certificateholders until they

are paid in full. During the accumu-

lation period, the investors’ share of

principal payments is paid into a

principal funding account designed

to accumulate amounts so that the

certificates can be paid in full on the

expected final payment date.

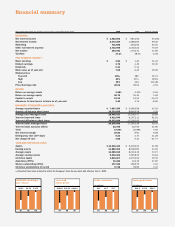

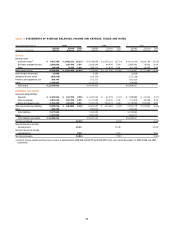

Table 2 indicates the impact of

the consumer loan securitizations on

average earning assets, net interest

margin and loan yield for the periods

presented. The Company intends to

continue to securitize consumer loans.

(in percentages)

8.81 9.91 10.83

97 98 99

managed net

interest margin

(in percentages)

15.73 16.99 17.59

97 98 99

managed loan

yield

table 2: OPERATING DATA AND RATIOS

Year Ended December 31 (Dollars in Thousands) 1999 1998 1997

Reported:

Average earning assets $ 9,694,406 $ 7,225,835 $ 5,753,997

Net interest margin 10.86% 9.51% 6.54%

Loan yield 19.33 18.75 15.11

Managed:

Average earning assets $ 20,073,964 $ 17,086,813 $ 14,658,143

Net interest margin 10.83% 9.91% 8.81%

Loan yield 17.59 16.99 15.73

RISK ADJUSTED REVENUE AND MARGIN

The Company’s products are designed with the objective of max-

imizing revenue for the level of risk undertaken. Management

believes that comparable measures for external analysis are the

risk adjusted revenue and risk adjusted margin of the managed

portfolio. Risk adjusted revenue is defined as net interest

income and non-interest income less net charge-offs. Risk

adjusted margin measures risk adjusted revenue as a percent-