Capital One 1999 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 1999 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

29

increased $311.1 million, or 83%, as average earning assets

increased 26% and the net interest margin increased to 9.51%

from 6.54%. The provision for loan losses increased $4.2 mil-

lion, or 2%, as the reported charge-off rate decreased to 4.24%

in 1998 from 4.83% in 1997, offset by average reported con-

sumer loans increasing 30%. Non-interest income increased

$419.2 million, or 39%, primarily due to the increase in aver-

age managed accounts of 39%. Increases in marketing

expenses of $221.4 million, or 98%, and salaries and benefits

expense of $187.1 million, or 65% reflect the increase in mar-

keting investment in existing and new product opportunities and

the cost of operations to manage the growth in the Company’s

accounts and products offered. Average managed consumer

loans grew 17% for the year ended December 31, 1998, to

$15.2 billion from $13.0 billion for the year ended December

31, 1997, and average accounts grew 39% for the same period

to 13.8 million from 9.9 million as a result of the continued suc-

cess of the Company’s marketing and account management

strategies.

MANAGED CONSUMER LOAN PORTFOLIO

The Company analyzes its financial performance on a managed

consumer loan portfolio basis. Managed consumer loan data

adds back the effect of off-balance sheet consumer loans. The

Company also evaluates its interest rate exposure on a man-

aged portfolio basis.

The Company’s managed consumer loan portfolio is com-

prised of reported and off-balance sheet loans. Off-balance

sheet loans are those which have been securitized and

accounted for as sales in accordance with Statement of Finan-

cial Accounting Standards (“SFAS”) No. 125, “Accounting for

Transfers and Servicing of Financial Assets and Extinguishments

of Liabilities” (“SFAS 125”), and are not assets of the Company.

Therefore, those loans are not shown on the balance sheet.

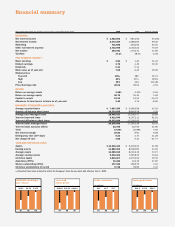

Table 1 summarizes the Company’s managed consumer

loan portfolio.

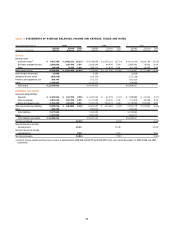

table 1: MANAGED CONSUMER LOAN PORTFOLIO

Year Ended December 31 (In Thousands) 1999 1998 1997 1996 1995

Year-End Balances:

Reported consumer loans $ 9,913,549 $ 6,157,111 $ 4,861,687 $ 4,343,902 $ 2,921,679

Off-balance sheet consumer loans 10,323,039 11,238,015 9,369,328 8,460,067 7,523,801

Total managed consumer loan portfolio $ 20,236,588 $ 17,395,126 $ 14,231,015 $ 12,803,969 $ 10,445,480

Average Balances:

Reported consumer loans $ 7,667,355 $ 5,348,559 $ 4,103,036 $ 3,651,908 $ 2,940,208

Off-balance sheet consumer loans 10,379,558 9,860,978 8,904,146 7,616,553 6,149,070

Total managed consumer loan portfolio $ 18,046,913 $ 15,209,537 $ 13,007,182 $ 11,268,461 $ 9,089,278

Since 1990, the Company has actively engaged in con-

sumer loan securitization transactions. Securitization involves

the transfer by the Company of a pool of loan receivables to an

entity created for securitizations, generally a trust or other spe-

cial purpose entity (“the trusts”). The credit quality of the

receivables is supported by credit enhancements, which may be

in various forms including a letter of credit, a cash collateral

guaranty or account, or a subordinated interest in the receiv-

ables in the pool. Certificates ($10.3 billion outstanding as of

December 31, 1999) representing undivided ownership inter-

ests in the receiv-

ables are sold to the

public through an

underwritten offering

or to private investors

in private placement

transactions. The Com-

pany receives the pro-

ceeds of the sale.

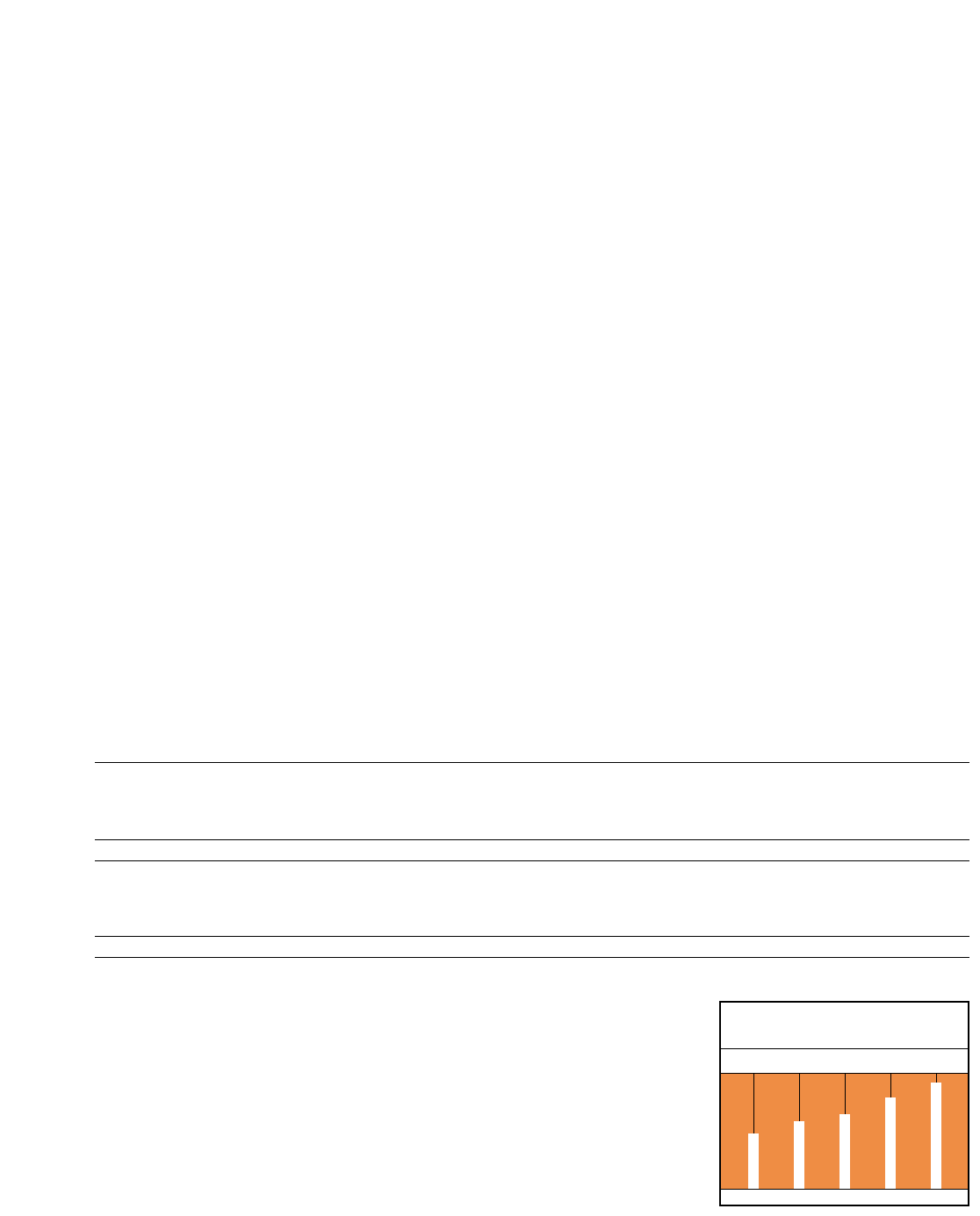

(in billions)

$10.4 $12.8 $14.2 $17.4 $20.2

95 96 97 98 99

managed loans