Capital One 1997 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 1997 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58

|

|

Notes to Consolidated Financial Statements (continued)

(Currencies in Thousands, Except Per Share Data)

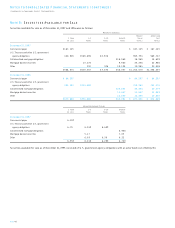

Note N: Significant Concentration of

Credit Risk

The Company is active in originating consumer loans primarily in

the United States.The Company reviews each potential customer’s

credit application and evaluates the applicant’s financial history

and ability and willingness to repay. Loans are made primarily on an

unsecured basis; however, certain loans require collateral in the

form of cash deposits. Foreign denominated consumer loans are

included in the “Other” geographic region loan category.The

geographic distribution of the Company’s consumer loans was

as follows:

Year Ended December 31

1997 1996

Geographic

Region: Loans % Loans %

South $ 5,061,414 35.57% $ 4,615,596 36.05%

Wes t 3,361,556 23.62 3,277,717 25.60

Northeast 2,835,256 19.92 2,465,237 19.25

Midwest 2,533,469 17.80 2,386,918 18.64

Other 439,320 3.09 58,501 .46

14,231,015 100.00% 12,803,969 100.00%

Less securitized

balances (9,369,328) (8,460,067)

Total loans $ 4,861,687 $ 4,343,902

Note O: Disclosures About Fair Value of

Financial Instruments

The following discloses the fair value of financial instruments as of

December 31, 1997 and 1996, whether or not recognized in the bal-

ance sheets, for which it is practical to estimate fair value. In cases

where quoted market prices are not available, fair values are based

on estimates using present value or other valuation techniques.

Those techniques are significantly affected by the assumptions used,

including the discount rate and estimates of future cash flows. In

that regard, the derived fair value estimates cannot be substanti-

ated by comparison to independent markets and, in many cases,

could not be realized in immediate settlement of the instrument. As

required under GAAP, these disclosures exclude certain financial

instruments and all nonfinancial instruments. Accordingly, the

aggregate fair value amounts presented do not represent the under-

lying value of the Company.

The following methods and assumptions were used by the Com-

pany in estimating the fair value as of December 31, 1997 and 1996,

for its financial instruments:

Cash and Cash Equivalents

The carrying amounts of cash and due from banks, federal funds

sold and resale agreements and interest-bearing deposits at other

banks approximated fair value.

Securities Available for Sale

The fair value of securities available for sale was determined using

current market prices. See Note B.

Consumer Loans

The net carrying amount of consumer loans, including the Com-

pany’s seller’s interest in securitized consumer loan receivables,

approximated fair value due to the relatively short average life and

variable interest rates on a substantial number of these loans.This

amount excluded any value related to account relationships.

Interest Receivable

The carrying amount approximated fair value.

Borrowings

The carrying amounts of interest-bearing deposits, other borrowings

and deposit notes approximated fair value.The fair value of senior

notes was $3,351,000 and $3,722,000 as of December 31, 1997 and

1996, respectively, determined based on quoted market prices.

Interest Payable

The carrying amount approximated fair value.

Swaps

The fair value was the estimated amount that the Company would

have received to terminate the swaps at the respective dates, taking

into account the forward yield curve. As of December 31, 1997 and

1996, the estimated fair value was $5,800 and $32,700, respectively.

PAGE 54