Capital One 1997 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 1997 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

|

|

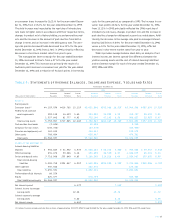

The Company measures exposure to its interest rate risk through

the use of a simulation model.The model generates a distribution of

possible twelve-month managed net interest income outcomes

based on (i) a set of plausible interest rate scenarios, as determined

by management based upon historical trends and market expecta-

tions, (ii) all existing financial instruments, including swaps, and

(iii) an estimate of ongoing business activity over the coming twelve

months.The Company’s asset/liability management policy requires

that based on this distribution there be at least a 95% probability

that managed net interest income achieved over the coming twelve

months will be no more than 4% below the mean managed net

interest income of the distribution. As of December 31, 1997, the

Company was in compliance with the policy; more than 95% of the

outcomes generated by the model produced a managed net interest

income of no more than 3.3% below the mean outcome.The inter-

est rate scenarios evaluated as of December 31, 1997 included

scenarios in which short-term interest rates rose by as much as

450 basis points or fell by as much as 250 basis points over

twelve months.

Implementation of this policy represents a change from the

asset/liability management policy in place as of December 31, 1996.

At that time, interest rate sensitivity was assessed on the basis of

the percent change in twelve-month managed net interest income

for an instantaneous and sustained 100 basis point rate shock

applied to an unchanging balance sheet. As of December 31, 1996,

the Company’s policy required that such a rate shock not result in

an adverse change of more than 5% in managed net interest

income; the exposure at the time was 2.1%.

The analysis does not consider the effects of the changed level of

overall economic activity associated with various interest rate sce-

narios. Further, in the event of a rate change of large magnitude,

management would likely take actions to further mitigate its expo-

sure to any adverse impact. For example, management may reprice

interest rates on outstanding credit card loans subject to the right

of the consumers in certain states to reject such repricing by giving

timely written notice to the Company and thereby relinquishing

charging privileges. However, the repricing of credit card loans may

be limited by competitive factors as well as certain legal constraints.

Interest rate sensitivity at a point in time can also be analyzed

by measuring the mismatch in balances of earning assets and inter-

est-bearing liabilities that are subject to repricing in future periods.

Table 12 reflects the interest rate repricing schedule for earning

assets and interest-bearing liabilities as of December 31, 1997.

PAGE 33

Table 12: Interest Rate Sensitivity

As of December 31, 1997 Subject to Repricing

Within >180 Days- >1 Year- Over

(Dollars in Millions) 180 days 1 year 5 Years 5 Years

Earning assets:

Federal funds sold $ 174

Interest-bearing deposits at other banks 59

Securities available for sale 438 $ 150 $ 604 $ 51

Consumer loans 2,454 213 2,195

Total earning assets 3,125 363 2,799 51

Interest-bearing liabilities:

Interest-bearing deposits 962 168 184

Other borrowings 561 235

Senior and other deposit notes 1,025 250 2,018 340

Total interest-bearing liabilities 2,548 653 2,202 340

Non-rate related assets (595)

Interest sensitivity gap 577 (290) 597 (884)

Impact of swaps 640 (215) (425)

Impact of consumer loan securitizations (4,418) 121 4,297

Interest sensitivity gap adjusted for impact of securitizations and swaps $(3,201) $ (169) $ 4,679 $(1,309)

Adjusted gap as a percentage of managed assets (19.48)% (1.03)% 28.47% (7.97)%

Adjusted cumulative gap $(3,201) $(3,370) $ 1,309

Adjusted cumulative gap as a percentage of managed assets (19.48)% (20.51)% 7.97% 0.00)%