BP 2008 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2008 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

BP Annual Report and Accounts 2008

Performance review

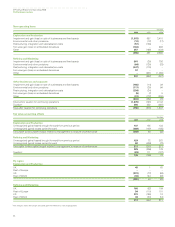

Recoverability of asset carrying values

BP assesses its fixed assets, including goodwill, for possible impairment

if there are events or changes in circumstances that indicate that carrying

values of the assets may not be recoverable and, as a result, charges for

impairment are recognized in the group’s results from time to time. Such

indicators include changes in the group’s business plans, changes in

commodity prices leading to unprofitable performance, low plant

utilization, evidence of physical damage and, for oil and gas properties,

significant downward revisions of estimated volumes or increases in

estimated future development expenditure. If there are low oil prices,

natural gas prices, refining margins or marketing margins during

an extended period, the group may need to recognize significant

impairment charges.

The assessment for impairment entails comparing the carrying

value of the cash-generating unit with its recoverable amount, that is,

the higher of fair value less costs to sell and value in use. Value in use

is usually determined on the basis of discounted estimated future

net cash flows.

Determination as to whether and how much an asset is impaired

involves management estimates on highly uncertain matters such as

future commodity prices, the effects of inflation on operating expenses,

discount rates, production profiles and the outlook for global or regional

market supply-and-demand conditions for crude oil, natural gas and

refined products.

For oil and natural gas properties, the expected future cash flows

are estimated based on the group’s plans to continue to develop and

produce proved reserves and associated risk-adjusted probable and

possible volumes. Expected future cash flows from the sale or

production of these volumes are calculated based on the management’s

best estimate of future oil and gas prices. Prices for oil and natural gas

used for future cash flow calculations are based on market prices for the

first five years and the group’s long-term planning assumptions

thereafter. As at 31 December 2008, the group’s long-term planning

assumptions were $75 per barrel for Brent and $7.50/mmBtu for Henry

Hub (2007 $60 per barrel and $7.50/mmBtu). These long-term planning

assumptions are subject to periodic review and modification. The

estimated future level of production is based on assumptions about

future commodity prices, lifting and development costs, field decline

rates, market demand and supply, economic regulatory climates and

other factors.

The future cash flows are adjusted for risks specific to the cash-

generating unit and are discounted using a pre-tax discount rate. The

discount rate is derived from the group’s post-tax weighted average cost

of capital and is adjusted where applicable to take into account any

specific risks relating to the country where the cash-generating unit is

located. Typically rates of 11% or 13% are used (2007 11% or 13%).

The rate applied in each country is re-assessed each year by analyzing

relevant information.

Irrespective of whether there is any indication of impairment,

BP is required to test annually for impairment of goodwill acquired in a

business combination. The group carries goodwill of approximately

$9.9 billion on its balance sheet, principally relating to the Atlantic

Richfield and Burmah Castrol acquisitions. In testing goodwill for

impairment, the group uses a similar approach to that described above.

If there are low oil prices or natural gas prices or refining margins or

marketing margins for an extended period, the group may need to

recognize significant goodwill impairment charges.

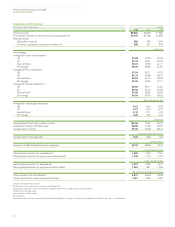

Taxation

The computation of the group’s income tax expense involves the

interpretation of applicable tax laws and regulations in many jurisdictions

throughout the world. The resolution of tax positions taken by the group,

through negotiations with relevant tax authorities or through litigation,

can take several years to complete and in some cases it is difficult to

predict the ultimate outcome.

In addition, the group has carry-forward tax losses in certain

taxing jurisdictions that are available to offset against future taxable

profit. However, deferred tax assets are recognized only to the extent

that it is probable that taxable profit will be available against which the

unused tax losses can be utilized. Management judgement is exercised

in assessing whether this is the case.

To the extent that actual outcomes differ from management’s

estimates, taxation charges or credits may arise in future periods. For

more information see Financial statements – Note 20 on page 135 and

Note 44 on page 174.

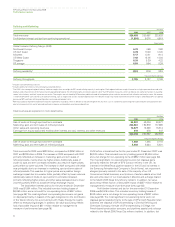

Derivative financial instruments

The group uses derivative financial instruments to manage certain

exposures to fluctuations in foreign currency exchange rates, interest

rates and commodity prices as well as for trading purposes. In addition,

derivatives embedded within other financial instruments or other host

contracts are treated as separate derivatives when their risks and

characteristics are not closely related to those of the host contract. All

such derivatives are initially recognized at fair value on the date on which

a derivative contract is entered into and are subsequently remeasured at

fair value. Gains and losses arising from changes in the fair value of

derivatives that are not designated as effective hedging instruments are

recognized in the income statement.

In some cases the fair values of derivatives are estimated using

models and other valuation methods due to the absence of quoted prices

or other observable, market-corroborated data. In particular, this applies

to the majority of the group’s natural gas and LNG embedded derivatives.

These are primarily long-term UK gas contracts that use pricing formulae

not related to gas prices, for example, oil product and power prices.

These contracts are valued using models with inputs that include price

curves for each of the different products that are built up from active

market pricing data and extrapolated to the expiry of the contracts using

the maximum available external pricing information. Additionally, where

limited data exists for certain products, prices are interpolated using

historic and long-term pricing relationships. Price volatility is also an input

for the models. Changes in the key assumptions could have a material

impact on the gains and losses on embedded derivatives recognized in

the income statement. For more information see Financial statements –

Note 34 on page 150. An analysis of the sensitivity of the fair value of the

natural gas and LNG derivatives to changes in the key assumptions is

provided in Financial statements – Note 28 on page 142.

62