Qantas 2015 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2015 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106

|

|

95

QANTAS ANNUAL REPORT 2015

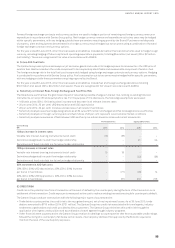

ii. Subsequent Expenditure

Subsequent expenditure is capitalised only if it is probable that the future economic benefits associated with the expenditure will

flow to the Group.

iii. Depreciation

Depreciation is provided on a straight-line basis on all items of property, plant and equipment except for freehold land, which is

not depreciated. The depreciation rates of owned assets are calculated so as to allocate the cost or valuation of an asset, less

any estimated residual value, over the asset’s estimated useful life to the Qantas Group. Assets are depreciated from the date of

acquisition or, with respect to internally constructed assets, from the time an asset is completed and available for use. The costs of

improvements to assets are depreciated over the remaining useful life of the asset or the estimated useful life of the improvement,

whichever is the shorter. Assets under finance lease are depreciated over the term of the relevant lease or, where it is likely the

Qantas Group will obtain ownership of the asset, the life of the asset.

The principal asset depreciation periods and estimated residual value percentages are:

Years

Residual Value

(%)

Buildings and leasehold improvements 10 – 40 01

Plant and equipment 3 – 20 0

Passenger aircraft and engines 2.5 – 20 0 – 10

Freighter aircraft and engines 2.5 – 20 0 – 20

Aircraft spare parts 15 – 20 0 – 20

1 Certain leases allow for the sale of leasehold improvements for fair value. In these instances, the expected fair value is used as the estimated residual value.

Useful lives and residual values are reviewed annually and reassessed having regard to commercial and technological developments,

the estimated useful life of assets to the Qantas Group and the long-term fleet plan.

iv. Maintenance and Overhaul Costs

An element of the cost of an acquired aircraft (owned and finance-leased aircraft) is attributed to its service potential, reflecting

the maintenance condition of its engines and airframe. This cost is depreciated over the shorter of the period to the next major

inspection event or the remaining life of the asset or remaining lease term.

The costs of subsequent major cyclical maintenance checks for owned and leased aircraft (including operating leases) are

recognised and depreciated over the shorter of the scheduled usage period to the next major inspection event or the remaining life

ofthe aircraft or lease term (as appropriate).

Maintenance checks which are covered by the third party maintenance agreements where there is a transfer of risk and legal

obligation are expensed on the basis of hours flown.

All other maintenance costs are expensed as incurred.

Modifications that enhance the operating performance or extend the useful lives of aircraft are capitalised and depreciated over the

remaining estimated useful life of the asset or remaining lease term (as appropriate). Manpower costs in relation to employees who

are dedicated to major modifications to aircraft are capitalised as part of the cost of the modification to which they relate.

v. Manufacturers’ Credits

The Qantas Group receives credits from manufacturers in connection with the acquisition of certain aircraft and engines. These

credits are recorded as a reduction to the cost of the related aircraft and engines. Where the aircraft are held under operating leases,

the credits are deferred and reduced from the operating lease rentals on a straight-line basis over the period of the related lease as

deferred credits.

vi. Capital Projects

Capital projects are disclosed within the categories to which they relate and are stated at cost. When the asset is ready for its

intended use, it is capitalised and depreciated.

(I) ASSETS CLASSIFIED AS HELD FOR SALE

Non-current assets or disposal groups comprising assets and liabilities that are expected to be recovered primarily through

sale rather than through continued use are classified as held for sale. Immediately before classification as held for sale, the

measurement of the assets or components of a disposal group is measured in accordance with the Qantas Group’s accounting

policies. Thereafter, the assets, or disposal group, are measured at the lower of carrying amount and fair value less costs to sell.

Anyimpairment of a disposal group is first allocated to goodwill and then to remaining assets and liabilities on a pro-rata basis,

except that no loss is allocated to inventories, financial assets or deferred tax assets. These continue to be measured in accordance

with the Qantas Group’s accounting policies. Impairment losses on initial classification as held for sale and subsequent gains or

losses on remeasurement are recognised in the Consolidated Income Statement.