Qantas 2015 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2015 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

|

|

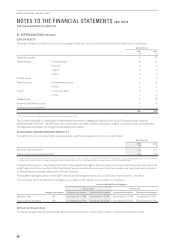

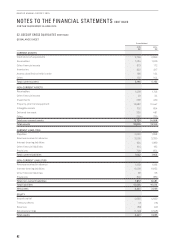

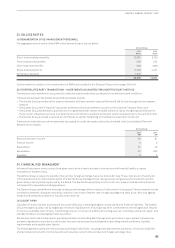

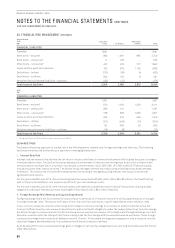

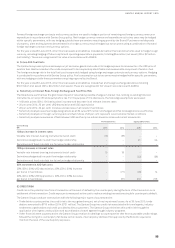

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

FOR THE YEAR ENDED 30 JUNE 2015

90

QANTAS ANNUAL REPORT 2015

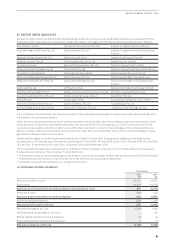

37. SIGNIFICANT ACCOUNTING POLICIES CONTINUED

The Group’s share of the associates’ post-acquisition profit or loss is recognised in the Consolidated Income Statement from the

date that significant influence commences until the date that significant influence ceases. The Group’s share of post-acquisition

movements in reserves is recognised in other comprehensive income. The cumulative post-acquisition movements are adjusted

against the carrying value of the investment.

Dividends reduce the carrying amount of the equity accounted investment.

When the Group’s share of losses exceeds the equity accounted carrying value of an associate, the Group’s carrying amount is

reduced to nil and recognition of further losses is discontinued, except to the extent that the Group has incurred legal or constructive

obligations to fund the associates’ operations or has made payments on behalf of an associate.

vi. ransactions Eliminated on Consolidation

Intra-group transactions, balances and unrealised gains and losses on transactions between controlled entities are eliminated

in preparing the Consolidated Financial Statements. Unrealised gains and losses arising from transactions with investments

accounted for under the equity method are eliminated to the extent of the Group’s interest in the associate.

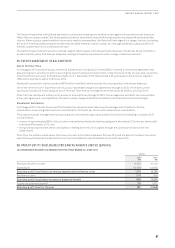

(B) FOREIGN CURRENCY

i. Foreign Currency Transactions

Transactions in foreign currencies are translated to the functional currency of the Group at the rates of exchange prevailing at the

date of each transaction except where hedge accounting is applied. At reporting date, monetary assets and liabilities denominated

in foreign currencies are translated to the functional currency at the rates of exchange prevailing at that date. Resulting exchange

differences are brought to account as exchange gains or losses in the Consolidated Income Statement in the year in which the

exchange rates change. Non-monetary assets and liabilities that are measured in terms of historical cost in a foreign currency

are translated using the exchange rate at the date of the transaction. Non-monetary assets and liabilities denominated in foreign

currencies that are stated at fair value are translated to the functional currency at foreign exchange rates prevailing at the dates the

fair value was determined.

ii. Foreign Operations

Assets and liabilities of foreign operations, including controlled entities and investments accounted for under the equity method,

are translated to the functional currency of the Group at the rates of exchange prevailing at balance date. The income statements of

foreign operations are translated to the functional currency at rates approximating the foreign exchange rates prevailing at the dates

of the transactions. Exchange differences arising on translation are recognised in other comprehensive income and are presented

within equity in the foreign currency translation reserve. When a foreign operation is disposed of such that control, significant

influence or joint control is lost, the cumulative amount in the translation reserve related to that foreign operation is reclassified to

the Consolidated Income Statement as part of the gain or loss on disposal. When the Group disposes of only part of its interest in

an investment accounted for under the equity method that includes a foreign operation, while retaining significant influence or joint

control, the relevant proportion of the cumulative amount is reclassified to the Consolidated Income Statement.

When the settlement of a monetary item receivable from or payable to a foreign operation is neither planned nor likely in the

foreseeable future, foreign exchange gains and losses arising from such a monetary item are considered to form part of the net

investment in a foreign operation and are recognised in other comprehensive income and are presented within equity in the foreign

currency translation reserve.

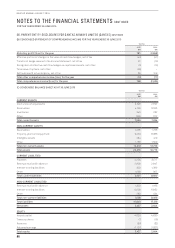

(C) FINANCIAL INSTRUMENTS

NON-DERIVATIVE FINANCIAL INSTRUMENTS

i. Recognition and Measurement of Non-derivative Financial Assets

The Group classifies non-derivative financial assets at initial recognition as either financial assets at fair value through profit and

loss or financial assets at amortised cost.

Financial assets at fair

value through profit

or loss

A financial asset is classified as at fair value through profit or loss if it is classified as held-for-trading

or is designated as such on initial recognition. Directly attributable transaction costs are recognised

in profit or loss as incurred. Financial assets at fair value through profit or loss are measured at fair

value and changes therein, including any interest or dividend income, are recognised in profit or loss.

Financial assets at

amortised cost

These assets are initially recognised at fair value plus any directly attributable transaction costs,

except for trade receivables which do not contain a significant financing component and are

recognised at transaction price. Subsequent to initial measurement, they are measured at amortised

cost using the effective interest rate method.