Loreal 2011 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2011 Loreal annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

|

|

95REGISTRATION DOCUMENT − L’ORÉAL 2011

2011 Consolidated Financial Statements

4

Notes to the consolidated nancial statements

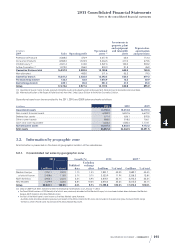

Sales incentives, cash discounts, provisions for returns and

incentives granted to customers are recorded simultaneously

to the recognition of the sales if they can be estimated in a

reasonably reliable manner, based on statistics compiled from

past experience and contractual conditions.

1.5. Cost of sales

The cost of goods sold consists mainly of the industrial

production cost of products sold, the cost of distributing

products to customers including freight and delivery costs, either

directly or indirectly through depots, inventory impairment costs,

and royalties paid to third parties.

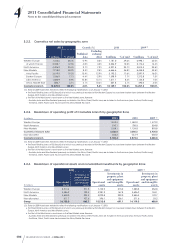

1.6. Research and development

expenditure

Expenditure during the research phase is charged to the

income statement for the financial year during which it is

incurred.

Expenses incurred during the development phase are

recognised as

Intangible assets

only if they meet all the following

criteria set out in IAS38:

♦the project is clearly defined and the related costs are

separately identified and reliably measured;

♦the technical feasibility of the project has been demonstrated;

♦the intention and ability to complete the project and to use

or sell the products resulting from the project have been

demonstrated;

♦the resources necessary to complete the project and to use

or sell it are available;

♦the Group can demonstrate that the project will generate

probable future economic benefits, as the existence of a

potential market for the production resulting from the project,

or its internal usefulness has been demonstrated.

In view of the very large number of development projects and

uncertainties concerning the decision to launch products

relating to these projects, L’Oréal considers that some of these

capitalisation criteria are not met.

The development costs of software for internal use are

capitalised for the programming, coding and testing phases.

The costs of substantial updates and upgrades resulting in

additional functions are also capitalised.

Capitalised development costs are amortised from the

date on which the software is made available in the entity

concerned over its probable useful life, which in most cases

is between 5 and 7years.

1.7. Advertising and promotion

expenses

These expenses consist mainly of expenses relating to the

advertisement and promotion of products to customers and

consumers. They are charged to the income statement for the

financial year in which they are incurred.

1.8. Selling, general and

administrative expenses

These expenses relate mainly to sales teams and sales team

management, marketing teams and administrative services, as

well as general expenses and the costs of share-based payment

(stock options and free shares).

1.9. Foreign exchange gains and

losses

Foreign exchange gains and losses resulting from the difference

between the value of foreign currency operating income and

expenses translated at the spot rate effective on the transaction

date and at the exchange rate effective on the settlement date

are recognised directly on the appropriate income and expense

lines, after allowing for hedging derivatives. Changes in the time

value of hedging derivatives (including option premiums) are

systematically charged to the income statement (note1.3).

1.10. Operating profit

Operating profit consists of gross profit less research and

development expenses, advertising and promotion expenses,

and selling, general and administrative expenses. Operating

profit corresponds to the definition of current operating profit

provided by

Conseil National de la Comptabilité

(CNC)

recommendation No.2009-R-03 of July2nd, 2009 regarding the

presentation of financial statements for companies applying

international accounting standards. It notably includes the

entire charge relating to the

Contribution Économique

Territoriale

(CET) tax collected in France, including its value-

added based component. The classification of the CET tax in

operating expenses is therefore consistent with the classification

of the former business tax

(taxe professionelle)

it replaces.

1.11. Other income and expenses

The

Other income and expenses item

includes capital gains

and losses on disposals of property, plant and equipment and

intangible assets, impairment of assets, restructuring costs, and

clearly identified, non-recurring income and expense items that

are material to the consolidated financial statements.

The cost of restructuring operations is fully provisioned if it results

from a Group obligation towards a third party originating from

a decision taken by a competent body which is announced

to the third parties concerned before the end of the reporting