Loreal 2011 Annual Report Download - page 187

Download and view the complete annual report

Please find page 187 of the 2011 Loreal annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

|

|

185REGISTRATION DOCUMENT − L’ORÉAL 2011

Corporate social, environmental and societal responsibility

6

Social information

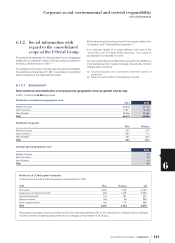

Employee B enefit and pension schemes and other

benefits

Depending on the legislation and practices in each country,

L’Oréal adheres to pension schemes, pre-retirement arrangements

and E mployee B enefit schemes offering a variety of additional

coverage for its employees.

In2002, L’Oréal set up a Supervisory Committee for pension

and E mployee B enefit schemes offered by its subsidiaries. This

committee ensures the implementation and the monitoring of

L’Oréal’s pension and E mployee B enefits policy as defined by the

L’Oréal Executive Committee.

This policy provides for general principles in the following

areas: definition and implementation of schemes, relations

with employees, financing and cost of the schemes, and

management of the schemes. Approval must first be obtained

from the Supervisory Committee prior to the introduction of any

new scheme or the modification of any existing scheme. The

Supervisory Committee works together closely with the operational

management of the d ivisions and zones.

The characteristics of the pension schemes and other pre-

retirement benefits offered by the subsidiaries outside France vary

depending on the applicable laws and regulations as well as the

practices of the companies in each country.

In many countries, L’Oréal participates in establishing additional

retirement benefits for its employees through a whole series of

defined benefit schemes and/or defined contribution schemes

(e.g. United States, the Netherlands, Belgium, Canada, and

Latin American countries). In some cases, the defined benefit

schemes have been closed to new recruits who are offered

defined contribution schemes (Germany, Belgium and the United

Kingdom). This series of defined benefit and defined contribution

schemes makes it possible to share the financial risks and ensure

improved cost stability. In defined contribution schemes, the

Company’s commitment mainly consists in paying a percentage

of the employee’s annual salary into a pension plan each year.

The defined benefit schemes are financed by payments into

specialist funds or by setting up provisions, in accordance with

the accounting standards adopted by L’Oréal. The performance

of the managers of the main funds established, as well as the

financial stability rating of the custodians, are regularly reviewed

by the Supervisory Committee.

Employee pension schemes in France

In France, L’Oréal has supplemented its retirement plan by creating

on January1st, 2001 a defined benefit scheme with conditional

entitlements based on the employee’s presence in the Company

at the end of his/her career. Then, on September1st, 2003, a defined

contribution scheme with accrued entitlements was introduced.

Defined benefit scheme

In order to provide additional cover, if applicable, to compulsory

pensions provided by the French Social Security compulsory

pension scheme, the ARRCO or AGIRC (mandatory French

supplementary pension schemes), L’Oréal introduced on

January1st, 2001, a defined benefit scheme with conditional

entitlements, the “Retirement Income Guarantee for former

Senior Managers”

(“Garantie de ressources des retraités anciens

cadres dirigeants”).

Prior to this, on December31st, 2000, L’Oréal

closed another defined benefit scheme, also with conditional

entitlements, the “Pension Cover of the Members of the Comité

de Conjoncture”

(“Garantie de retraite des membres du Comité

de Conjoncture”).

Access to the “Retirement Income Guarantee for former Senior

Managers”, created on January1st, 2001, is open to former L’Oréal

Senior Managers who fulfil, in addition to having ended their career

with the Company, the condition of having had the status of Senior

Manager within the meaning of ArticleL.3111-2 of the French

Labour Code for at least ten years at the end of their career.

This scheme provides entitlement to payment to the beneficiary

retiree of a Life Annuity, as well as, after his/her death, the

payment to the beneficiary’s spouse and/or ex-spouse (s) of

a surviving Spouse Pension and, to the children, of an Orphan

Pension, subject to the children fulfilling certain conditions. The

calculation basis for the Guaranteed Income is the average of

the salaries for the best three years out of the seven calendar

years prior to the end of the Senior Manager’s career at L’Oréal.

The Guaranteed Income is calculated based on the beneficiary’s

number of years of professional activity in the Company at the

date of the end of his/her career at L’Oréal, and limited to a

maximum of 25years, each year leading to a steady, gradual

increase of 1.8% in the level of the Guarantee. At this date,

the gross Guaranteed Income may not exceed 50% of the

calculation basis for the Guaranteed Income, nor exceed the

average of the fixed part of the salaries for the three years used

for the calculation basis. A gross annuity and gross Lump Sum

Equivalent are then calculated taking into account the sum

of the annual pensions accrued on the date when the retiree

applies for his/her pension as a result of his/her professional

activity and on the basis of a beneficiary who is 65years of age.

The Life Annuity is the result of the conversion into an annuity

at the beneficiary’s age on the date he/she applies for his/her

pension of the gross Lump Sum Equivalent, less the amount of

all payments due as a result of termination of the employment

contract, excluding any paid notice period and paid holiday

and less all salaries paid under an early retirement leave plan,

if such lump sum equivalent is the result of these operations.

Around 450Senior Managers are eligible for this scheme, subject

to their fulfilling all the conditions after having ended their career

with the Company.

Access to the Pension Cover for Members of the “Comité de

Conjoncture” has been closed since December31st, 2000.

This former scheme granted entitlement to payment to the

beneficiary retiree, after having ended his/her career with the

Company, of a Life Annuity as well as, after his/her death, the

payment to the spouse and/or ex-spouse (s) of a surviving Spouse

Pension and, to the children, of an Orphan Pension, subject to

the children fulfilling certain conditions. The calculation basis

for the Pension Cover is the average of the salaries for the best

three years out of the seven calendar years prior to the end of the

beneficiary’s career at L’Oréal. The Pension Cover is calculated

on the basis of the beneficiary’s number of years’ service and

limited to a maximum of 40years, it being specified that at the date

of closure of the scheme, on December31st, 2000, the minimum

length of service required was 10years. The Pension Cover may

not exceed 40% of the calculation basis for the Pension Cover,

plus 0,5% per year for the first twenty years, then 1% per year for the

following twenty years, nor exceed the average of the fixed part

of the salaries for the three years used for the calculation basis.

Around 120Senior Managers (active or retired) are eligible for this

scheme subject to the condition, for those in active employment,

of fulfilling all the conditions after having ended their career with

the Company.