ICICI Bank 2015 Annual Report Download - page 201

Download and view the complete annual report

Please find page 201 of the 2015 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

forming part of the Consolidated Accounts (Contd.)

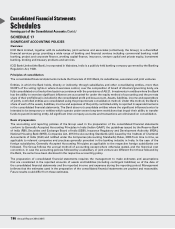

Schedules

199Annual Report 2014-2015

Consolidated Financial Statements

been accounted for as per the Guidance Note on Accounting for Leases issued by ICAI. The finance leases entered

post April 1, 2001 have been accounted for as per Accounting Standard 19 - Leases.

Income on discounted instruments is recognised over the tenure of the instrument.

Dividend income is accounted on an accrual basis when the right to receive the dividend is established.

Loan processing fee is accounted for upfront when it becomes due except in the case of foreign banking

subsidiaries, where it is amortised over the period of the loan.

Project appraisal/structuring fee is accounted for on the completion of the agreed service.

Arranger fee is accounted for as income when a significant portion of the arrangement/syndication is completed.

Commission received on guarantees issued is amortised on a straight-line basis over the period of the guarantee.

Fund management and portfolio management fees are recognised on an accrual basis.

All other fees are accounted for as and when they become due.

The Bank deals in bullion business on a consignment basis. The difference between price recovered from

customers and cost of bullion is accounted for at the time of sale to the customers. The Bank also deals in bullion

on a borrowing and lending basis and the interest paid/received is accounted on accrual basis.

Income from securities brokerage activities is recognised as income on the trade date of the transaction. Brokerage

income in relation to public or other issuances of securities is recognised based on mobilisation and terms of

agreement with the client.

Life insurance premium for non-linked policies is recognised as income when due from policyholders. For unit linked

business, premium is recognised when the associated units are created. Premium on lapsed policies is recognised

as income when such policies are reinstated. Top-up premiums paid by unit linked policyholders’ are considered as

single premium and recognised as income when the associated units are created. Income from unit linked policies,

which includes fund management charges, policy administration charges, mortality charges and other charges, if

any, are recovered from the linked funds in accordance with the terms and conditions of the policy and are recognised

when due.

In the case of general insurance business, premium is recorded for the policy period at the commencement of risk

and for instalment cases, it is recorded on instalment due dates. Premium earned is recognised as income over

the period of the risk or the contract period based on 1/365 method, whichever is appropriate, on a gross basis,

net of service tax. Any subsequent revision to premium is recognised over the remaining period of risk or contract

period. Adjustments to premium income arising on cancellation of policies are recognised in the period in which

the policies are cancelled. Commission on re-insurance ceded is recognised as income in the period of ceding the

risk. Profit commission under re-insurance treaties, wherever applicable, is recognised as income in the period of

final determination of profits and combined with commission on reinsurance ceded.

In case of life insurance business, reinsurance premium ceded is accounted in accordance with the terms of the

relevant treaty with the reinsurer. Profit commission on reinsurance ceded is netted off against premium ceded on

reinsurance.

In the case of general insurance business, insurance premium on ceding of the risk is recognised in the period in

which the risk commences. Any subsequent revision to premium ceded is recognised in the period of such revision.

Adjustment to re-insurance premium arising on cancellation of policies is recognised in the period in which they

are cancelled. In case of life insurance business, reinsurance premium ceded is accounted in accordance with the

terms and conditions of the relevant treaties with the reinsurer. Profit commission on reinsurance ceded is netted

off against premium ceded on reinsurance.

In the case of general insurance business, premium deficiency is recognised when the sum of expected claim

costs and related expenses and maintenance costs exceed the reserve for unexpired risks and is computed at a

company level. The expected claim cost is calculated and duly certified by the Appointed Actuary.