ICICI Bank 2015 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2015 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

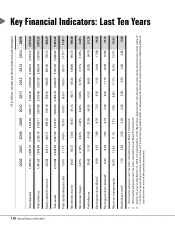

103Annual Report 2014-2015

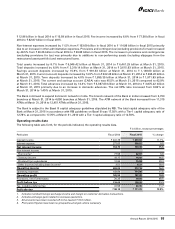

Credit risk RWA increased by ` 332.43 billion from ` 4,409.13 billion at March 31, 2014 to ` 4,741.56 billion at

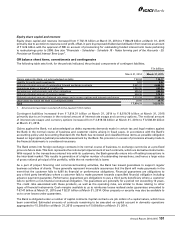

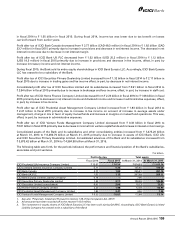

March 31, 2015 primarily due to increase of ` 324.61 billion in RWA for on-balance sheet assets and increase of

` 7.82 billion in RWA for off-balance sheet assets.

Market risk RWA increased by ` 68.49 billion from ` 265.74 billion at March 31, 2014 to ` 334.23 billion at March 31, 2015

primarily due to increase in fixed rate investments and investment in government securities with longer tenor.

The operational risk RWA at March 31, 2015 is ` 373.17 billion (capital charge of ` 33.58 billion). The operational risk capital

charge is computed based on 15% of average of previous three financial years’ gross income and is revised on an annual

basis at June 30.

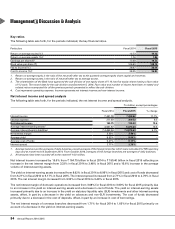

Internal assessment of capital

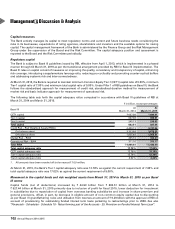

The capital management framework of the Bank includes a comprehensive internal capital adequacy assessment process

conducted annually, which determines the adequate level of capitalisation necessary to meet regulatory norms and

current and future business needs, including under stress scenarios. The internal capital adequacy assessment process

is formulated at both standalone bank level and the consolidated group level. The internal capital adequacy assessment

process encompasses capital planning for a four year time horizon, identification and measurement of material risks and

the relationship between risk and capital.

The capital management framework is complemented by the risk management framework, which includes a

comprehensive assessment of material risks. Stress testing, which is a key aspect of the internal capital adequacy

assessment process and the risk management framework, provides an insight on the impact of extreme but plausible

scenarios on the Bank’s risk profile and capital position. Based on the Bank’s Board-approved stress testing framework,

the Bank conducts stress tests on various portfolios and assesses the impact on the capital ratios and the adequacy of

capital buffers for current and future periods. The Bank periodically assesses and refines its stress tests in an effort to

ensure that the stress scenarios capture material risks as well as reflect possible extreme market moves that could arise

as a result of market conditions. The business and capital plans and the stress testing results of the group entities are

integrated into the internal capital adequacy assessment process.

Based on the internal capital adequacy assessment process, the Bank determines the level of capital that needs to be

maintained by considering the following in an integrated manner:

strategic focus, business plan and growth objectives;

regulatory capital requirements as per RBI guidelines;

assessment of material risks and impact of stress testing;

perception of credit rating agencies, shareholders and investors;

future strategy with regard to investments or divestments in subsidiaries; and

evaluation of options to raise capital from domestic and overseas markets, as permitted by RBI from time to time.

The Bank continues to monitor further developments and believe that its current robust capital adequacy position and

demonstrated track record of access to domestic and overseas markets for capital raising will enable it to maintain the

necessary levels of capital as required by regulations while continuing to grow its business.

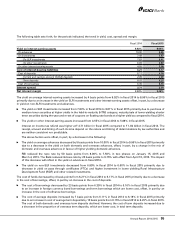

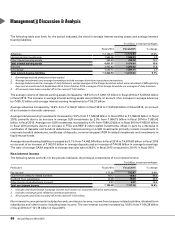

ASSET QUALITY AND COMPOSITION

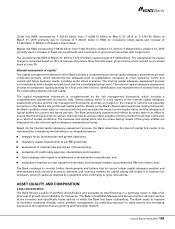

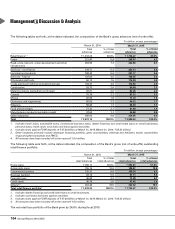

Loan concentration

The Bank follows a policy of portfolio diversification and evaluates its total financing in a particular sector in light of its

forecasts of growth and profitability for that sector. The Bank’s Credit Risk Management Group monitors all major sectors

of the economy and specifically tracks sectors in which the Bank has loans outstanding. The Bank seeks to respond

to economic weakness through active portfolio management, by restricting exposure to weak sectors and increasing

exposure to the segments that are growing and have been resilient.