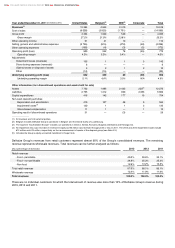

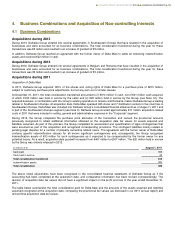

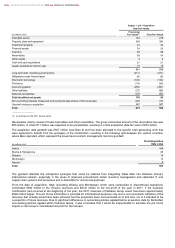

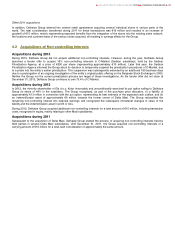

Food Lion 2013 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2013 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

Share Capital and Treasury Shares

Ordinary shares: Delhaize Group’s ordinary shares are classified as equity. Incremental costs directly attributable to the

issuance of ordinary shares and share options are recognized as a deduction from equity, net of any tax effects.

Treasury shares: Shares of the Group purchased by the Group or companies within the Group are included in equity at cost

(including any costs directly attributable to the purchase of the shares) until the shares are cancelled, sold or otherwise

disposed. Where such shares are subsequently reissued, any consideration received, net of any directly attributable

incremental transaction costs and the related income tax effects, is included in equity attributable to the company’s equity

holders.

Income Taxes

The tax expense for the period comprises current and deferred tax. Tax is recognized in the income statement except to the

extent that it relates to items recognized directly in OCI or equity.

The current income tax expense is calculated on the basis of the tax laws enacted or substantively enacted at the balance sheet

date in the countries where the Group operates and generates taxable income. Provisions and receivables are established on

the basis of amounts expected to be paid to or recovered from the tax authorities.

Deferred tax liabilities and assets are recognized, using the liability method, on temporary differences arising between the

carrying amount in the consolidated financial statements and the tax basis of assets and liabilities. However, the deferred income

tax is not accounted for if it arises from initial recognition of an asset or liability in a transaction other than a business combination

that at the time of the transaction affects neither accounting nor taxable profit or loss. Deferred income tax is determined

considering (i) tax rates and laws that have been enacted or substantively enacted at the balance sheet date that are expected to

apply when the temporary differences reverse and (ii) the expected manner of realization or settlement of the carrying amount of

assets and liabilities.

Deferred tax liabilities are recognized for temporary differences arising on investments in subsidiaries, associates and interests in

joint ventures, if any, except where the Group is able to control the timing of the reversal of the temporary difference and it is

probable that the temporary difference will not reverse in the foreseeable future.

A deferred tax asset is recognized only to the extent that it is probable that future taxable profit will be available against which the

temporary difference can be utilized. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that

it is no longer probable that the related tax benefit will be realized.

Deferred tax assets and liabilities are only offset if there is a legally enforceable right to offset current tax liabilities and assets

and the deferred income taxes relate to the same taxable entity and the same taxation authority.

The Group elected to present interests and penalties relating to income taxes in “Income tax expense” in the income statement.

Provisions

Provisions are recognized when the Group has a present legal or constructive obligation as a result of past events, it is more

likely than not that an outflow of resources will be required to settle the obligation, and the amount can be reliably estimated.

Provisions are measured at balance sheet date at management’s best estimate of the expenditures expected to be required to

settle the obligation, discounted using a pre-tax discount rate that reflects the current market assessments of the time value of

money and the risk specific to the liability, if material. Where discounting is used, the increase in the provision due to the passage

of time (“unwinding of the discount”) is recognized in “Finance costs” (see Note 29.1).

Closed store provisions: Delhaize Group regularly reviews its stores operating performance and assesses the Group’s plans

for certain store closures. Closing stores results in a number of activities required by IFRS in order to appropriately reflect

the value of assets and liabilities and related store closing costs, such as a review of net realizable value of inventory or

review for impairment of assets or CGUs (for both activities see the accounting policies described above). In addition,

Delhaize Group recognizes “Closed store provisions”, which consist primarily of provisions for onerous contracts and

severance (“termination”) costs (for both see further below). Costs recognized as part of store closings are included in “Other

operating expenses” (see Note 28), except for inventory write-downs, which are classified as “Cost of sales” (see Note 25). If

appropriate (see also “Non-Current Assets / Disposal Groups and Discontinued Operations” above), closed stores are

accounted for as assets held for sale and / or discontinued operations.

Onerous contracts: A provision is recognized for a present obligation arising under an onerous contract, which is defined as

a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits

expected to be received under it. Judgment is required in determining if a present obligation exists, taking into account all

available evidence. Once the existence has been established, at the latest upon actual closing of a store, Delhaize Group

recognizes provisions for the present value of the amount by which the unavoidable costs to fulfill the agreements exceed

the expected benefits from such agreements, which comprises the estimated non-cancellable lease payments, including

contractually required real estate taxes, common area maintenance and insurance costs, net of anticipated subtenant

income. The adequacy of the closed store provision is dependent upon the economic conditions in which stores are located

which will impact the Group’s ability to realize estimated sublease income. Owned and finance leased stores that are closed

and rented to third parties are reclassified as investment property (see Note 9).

When termination costs are incurred in connection with a store closing, a liability for the termination benefits is recognized in

accordance with IAS 19 Employee Benefits, at the earlier of the following dates: (a) when the Group can no longer withdraw

DELHAIZE GROUP ANNUAL REPORT 2013 FINANCIAL STATEMENTS

87