Entergy 2006 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2006 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

ENTERGY CORPORATION AND SUBSIDIARIES 2

2000066

46

■FUTURE OPERATING COSTS – Entergy assumes relatively minor

annual increases in operating costs. Technological or regulatory

changes that have a significant impact on operations could cause

a significant change in these assumptions.

In the fourth quarter of 2005, Entergy recorded a charge of $39.8

million ($25.8 million net-of-tax) as a result of the impairment of the

Competitive Retail Services business’ information technology sys-

tems. Entergy decided to divest the retail electric portion of the

Competitive Retail Services business operating in the ERCOT region

of Texas and, in connection with that decision, management evaluat-

ed the carrying amount of the Competitive Retail Services business’

information technology systems and determined that an impairment

provision should be recorded.

In the fourth quarter of 2004, Entergy recorded a charge of approxi-

mately $55 million ($36 million net-of-tax) as a result of an impairment

of the value of the Warren Power plant. Entergy concluded that the value

of the plant, which is owned in the non-nuclear wholesale assets busi-

ness, was impaired. Entergy reached this conclusion based on valuation

studies prepared in connection with the Entergy Asset Management

stock sale discussed above in “Results of Operations.”

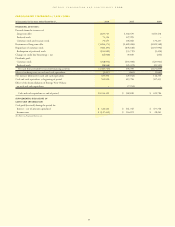

QUALIFIED PENSION AND OTHER POSTRETIREMENT BENEFITS

Entergy sponsors qualified, defined benefit pension plans which cover

substantially all employees. Additionally, Entergy currently provides

postretirement health care and life insurance benefits for substantially all

employees who reach retirement age while still working for Entergy.

Entergy’s reported costs of providing these benefits, as described in Note

11 to the consolidated financial statements, are impacted by numerous

factors including the provisions of the plans, changing employee demo-

graphics, and various actuarial calculations, assumptions, and accounting

mechanisms. Because of the complexity of these calculations, the long-

term nature of these obligations, and the importance of the assumptions

utilized, Entergy’s estimate of these costs is a critical accounting estimate

for the Utility and Non-Utility Nuclear segments.

Assumptions

Key actuarial assumptions utilized in determining these costs include:

■Discount rates used in determining the future benefit obligations;

■Projected health care cost trend rates;

■Expected long-term rate of return on plan assets; and

■Rate of increase in future compensation levels.

Entergy reviews these assumptions on an annual basis and adjusts

them as necessary. The falling interest rate environment and worse-

than-expected performance of the financial equity markets in previous

years have impacted Entergy’s funding and reported costs for these

benefits. In addition, these trends have caused Entergy to make a

number of adjustments to its assumptions.

In selecting an assumed discount rate to calculate benefit obliga-

tions, Entergy reviews market yields on high-quality corporate debt

and matches these rates with Entergy’s projected stream of benefit

payments. Based on recent market trends, Entergy increased its dis-

count rate used to calculate benefit obligations from 5.9% in 2005 to

6.00% in 2006. Entergy’s assumed discount rate used to calculate the

2004 benefit obligations was 6.00%. Entergy reviews actual recent

cost trends and projected future trends in establishing health care cost

trend rates. Based on this review, Entergy’s health care cost trend rate

assumption used in calculating the December 31, 2006 accumulated

postretirement benefit obligation was a 10% increase in health care

costs in 2007 gradually decreasing each successive year, until it reaches a

4.5% annual increase in health care costs in 2012 and beyond.

In determining its expected long-term rate of return on plan assets,

Entergy reviews past long-term performance, asset allocations, and

long-term inflation assumptions. Entergy targets an asset allocation

for its pension plan assets of roughly 65% equity securities, 31%

fixed-income securities and 4% other investments. The target alloca-

tion for Entergy’s other postretirement benefit assets is 51% equity

securities and 49% fixed-income securities. Entergy’s expected long-

term rate of return on plan assets used to calculate benefit obligations

was 8.5% in 2006, 2005 and 2004. The assumed rate of increase in

future compensation levels used to calculate benefit obligations was

3.25% in 2006, 2005 and 2004.

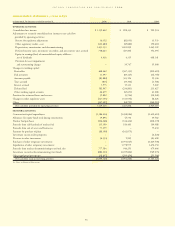

Cost Sensitivity

The following chart reflects the sensitivity of qualified pension cost to

changes in certain actuarial assumptions (dollars in thousands):

Impact on Impact on

Actuarial Change in 2006 Qualified Qualified Projected

Assumption Assumption Pension Cost Benefit Obligation

Increase/(Decrease)

Discount rate (0.25%) $11,746 $110,087

Rate of return

on plan assets (0.25%) $ 5,311 –

Rate of increase

in compensation 0.25% $ 6,034 $ 33,326

The following chart reflects the sensitivity of postretirement

benefit cost to changes in certain actuarial assumptions (dollars

in thousands):

Impact on

Impact on 2006 Accumulated

Actuarial Change in Postretirement Postretirement

Assumption Assumption Benefit Cost Benefit Obligation

Increase/(Decrease)

Health care

cost trend 0.25% $5,294 $25,774

Discount rate (0.25%) $3,510 $31,008

Each fluctuation above assumes that the other components of the

calculation are held constant.

Accounting Mechanisms

In September 2006, FASB issued SFAS 158, “Employer’s Accounting

for Defined Benefit Pension and Other Postretirement Plans, an

amendment of FASB Statements Nos. 87, 88, 106 and 132(R),” to be

effective December 31, 2006. SFAS 158 requires an employer to rec-

ognize in its balance sheet the funded status of its benefit plans. Refer

to Note 11 to the financial statements for a further discussion of SFAS

158 and Entergy’s funded status.

In accordance with SFAS No. 87, “Employers’ Accounting for

Pensions,” Entergy utilizes a number of accounting mechanisms that

reduce the volatility of reported pension costs. Differences between

actuarial assumptions and actual plan results are deferred and are

amortized into expense only when the accumulated differences exceed

10% of the greater of the projected benefit obligation or the market-

related value of plan assets. If necessary, the excess is amortized over

the average remaining service period of active employees.

Additionally, Entergy accounts for the effect of asset performance

on pension expense over a twenty-quarter phase-in period through a

“market-related” value of assets calculation. Since the market-related

value of assets recognizes investment gains or losses over a twenty-

quarter period, the future value of assets will be impacted as

previously deferred gains or losses are recognized.

Entergy’s qualified pension accumulated benefit obligation at

December 31, 2005 exceeded plan assets. As a result, Entergy was

required to recognize an additional minimum pension liability as

prescribed by SFAS 87. At December 31, 2005, Entergy’s qualified

pension plans’ additional minimum pension liability was $406 million

($382 million net of related pension assets). Other comprehensive

income was $15 million at December 31, 2005, after reductions for

the unrecognized prior service cost, amounts recoverable in rates, and

taxes. Net income for 2005 and 2004 was not affected. In accordance

with SFAS 158, the additional minimum pension liability has been

replaced in 2006 with the recording of the funded status of the defined

benefit and other postretirement benefit plans.

MANAGEMENT’S FINANCIAL DISCUSSION and ANALYSIS continued