Entergy 2006 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2006 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

|

|

ENTERGY CORPORATION AND SUBSIDIARIES 2

2000066

84

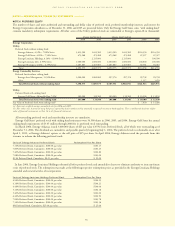

QUALIFIED PENSION OBLIGATIONS,PLAN ASSETS,FUNDED STATUS,

AMOUNTS NOT YET RECOGNIZED AND RECOGNIZED IN THE BALANCE

SHEET FOR ENTERGY CORPORATION AND ITS SUBSIDIARIES AS OF

DECEMBER 31, 2006 AND 2005 (IN THOUSANDS):

2006 2005

Change in Projected Benefit Obligation (PBO)

Balance at beginning of year $2,894,008 $ 2,555,086

Service cost 92,706 82,520

Interest cost 167,257 155,477

Amendments – 6,467

Actuarial loss 4,372 211,194

Employee contributions 1,003 1,032

Benefits paid (123,272) (117,768)

Balance at end of year $3,036,074 $ 2,894,008

Change in Plan Assets

Fair value of assets at beginning of year $1,994,879 $ 1,841,929

Actual return on plan assets 270,976 137,885

Employer contributions 318,470 131,801

Employee contributions 1,003 1,032

Benefits paid (123,272) (117,768)

Fair value of assets at end of year $2,462,056 $ 1,994,879

Funded status $(574,018) $ (899,129)

Amounts not yet recognized in the balance sheet

(before application of SFAS 158)

Unrecognized prior service cost $ 23,932 $ 29,393

Unrecognized net loss 580,880 713,285

Prepaid/(accrued) pension cost

recognized in the balance sheet $ 30,794 $ (156,451)

Amounts recognized in the balance sheet

(before application of SFAS 158)

Additional minimum pension liability $ (267,003) $ (406,463)

Intangible asset 5,336 24,159

Accumulated OCI (before taxes) 38,273 24,243

Regulatory asset 223,394 358,061

Net amount recognized $ 30,794 $ (156,451)

Change in amount recognized due to SFAS 158

Funded status $ (574,018)

Less: Prepaid/(accrued) pension cost recognized

in the balance sheet before application of

SFAS 158 30,794

Less: Additional minimum pension liability

before application of SFAS 158 (267,003)

Change in amount recognized due to

SFAS 158 $ (337,809)

Amount recognized in the balance sheet

(funded status under SFAS 158)

Non-current liabilities $ (574,018)

Amounts recognized in regulatory assets

Prior service cost $ 14,388

Net loss/(gain) 498,502

Total $ 512,890

Amounts recognized in OCI (before tax)

Prior service cost $ 9,544

Net loss/(gain) 82,378

Total $ 91,922

OTHER POSTRETIREMENT BENEFITS

Entergy also currently provides health care and life insurance benefits

for retired employees. Substantially all employees may become eligible

for these benefits if they reach retirement age while still working for

Entergy. Entergy uses a December 31 measurement date for its postre-

tirement benefit plans.

Effective January 1, 1993, Entergy adopted SFAS 106, which

required a change from a cash method to an accrual method

of accounting for postretirement benefits other than pensions.

At January 1, 1993, the actuarially determined accumulated

postretirement benefit obligation (APBO) earned by retirees

and active employees was estimated to be approximately

$241.4 million for Entergy (other than Entergy Gulf States) and

$128 million for Entergy Gulf States. Such obligations are being

amortized over a 20-year period that began in 1993. For the most

part, the Registrant Subsidiaries recover SFAS 106 costs from cus-

tomers and are required to contribute postretirement benefits

collected in rates to an external trust.

Entergy Arkansas, the portion of Entergy Gulf States regulated by

the PUCT, Entergy Mississippi, and Entergy New Orleans have

received regulatory approval to recover SFAS 106 costs through rates.

Entergy Arkansas began recovery in 1998, pursuant to an APSC

order. This order also allowed Entergy Arkansas to amortize a regula-

tory asset (representing the difference between SFAS 106 costs and

cash expenditures for other postretirement benefits incurred for a five-

year period that began January 1, 1993) over a 15-year period that

began in January 1998.

The LPSC ordered the portion of Entergy Gulf States regulated by

the LPSC and Entergy Louisiana to continue the use of the pay-as-

you-go method for ratemaking purposes for postretirement benefits

other than pensions. However, the LPSC retains the flexibility to

examine individual companies’ accounting for postretirement benefits

to determine if special exceptions to this order are warranted.

Pursuant to regulatory directives, Entergy Arkansas, Entergy

Mississippi, Entergy New Orleans, the portion of Entergy Gulf States

regulated by the PUCT, and System Energy contribute the postretire-

ment benefit obligations collected in rates to trusts. System Energy is

funding, on behalf of Entergy Operations, postretirement benefits

associated with Grand Gulf.

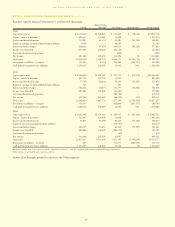

COMPONENTS OF NET OTHER POSTRETIREMENT BENEFIT COST

Total 2006, 2005, and 2004 other postretirement benefit costs of

Entergy Corporation and its subsidiaries, including amounts capitalized

and deferred, included the following components (in thousands):

2006 2005 2004

Service cost – benefits earned

during the period $ 41,480 $ 37,310 $ 30,947

Interest cost on APBO 57,263 51,883 53,801

Expected return on assets (19,024) (17,402) (18,825)

Amortization of transition obligation 2,169 3,368 9,429

Amortization of prior service cost (14,751) (13,738) (5,222)

Recognized net (gain)/loss 22,789 22,295 15,546

Net other postretirement benefit cost $ 89,926 $ 83,716 $ 85,676

Estimated amortization amounts from the regulatory asset or OCI to

net periodic cost in the following year (in thousands):

Transition obligation $ 3,831

Prior service cost $(15,837)

Net loss/(gain) $ 18,974

NOTESto CONSOLIDATED FINANCIAL STATEMENTS continued