Entergy 2006 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2006 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

|

|

ENTERGY CORPORATION AND SUBSIDIARIES 2

2000066

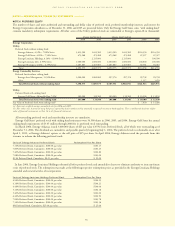

OTHER POSTRETIREMENT BENEFIT OBLIGATIONS,PLAN ASSETS,FUNDED

STATUS,AND AMOUNTS NOT YET RECOGNIZED AND RECOGNIZED IN THE

BALANCE SHEET OF ENTERGY CORPORATION AND ITS SUBSIDIARIES AS OF

DECEMBER 31, 2006 AND 2005 (IN THOUSANDS):

2006 2005

Change in APBO

Balance at beginning of year $ 997,969 $ 928,217

Service cost 41,480 37,310

Interest cost 57,263 51,883

Plan amendments (10,708) (64,200)

Plan participant contributions 6,904 6,749

Actuarial loss/(gain) (17,838) 98,041

Benefits paid (62,314) (60,031)

Medicare Part D subsidy received 1,610 –

Balance at end of year $1,014,366 $ 997,969

Change in Plan Assets

Fair value of assets at beginning of year $ 234,516 $ 214,005

Actual return on plan assets 27,912 15,003

Employer contributions 64,058 58,790

Plan participant contributions 6,904 6,749

Benefits paid (60,700) (60,031)

Fair value of assets at end of year $ 272,690 $ 234,516

Funded status $ (741,676) $(763,453)

Amounts not yet recognized in the balance sheet

(before application of SFAS 158)

Unrecognized transition obligation 13,007 15,176

Unrecognized prior service cost (62,062) (66,105)

Unrecognized net loss 353,733 403,252

Accrued other post retirement

benefit cost recognized $ (436,998) $(411,130)

Amounts recognized in the balance sheet (SFAS 158)

Current liabilities $ (27,372)

Non-current liabilities (714,304)

Total funded status $ (741,676)

Change in amount recognized

due to SFAS 158 $ (304,678)

Amounts recognized in regulatory assets (before tax)

Transition obligation $8,686

Prior service cost (9,263)

Net loss/(gain) 195,567

Total $ 194,990

Amounts recognized in OCI (before tax)

Transition obligation $4,321

Prior service cost (52,799)

Net loss/(gain) 158,166

Total $ 109,688

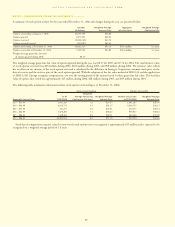

QUALIFIED PENSION AND OTHER POSTRETIREMENT PLANS’ASSETS

Entergy’s qualified pension and postretirement plans weighted-aver-

age asset allocations by asset category at December 31, 2006 and

2005 are as follows:

Qualified Pension Postretirement

2006 2005 2006 2005

Domestic Equity Securities 43% 45% 37% 37%

International Equity Securities 21% 21% 14% 15%

Fixed-Income Securities 34% 32% 49% 47%

Other 2% 2% –% 1%

The Plan Administrator’s trust asset investment strategy is to invest

the assets in a manner whereby long-term earnings on the assets (plus

cash contributions) provide adequate funding for retiree benefit

payments. The mix of assets is based on an optimization study that

identifies asset allocation targets in order to achieve the maximum

return for an acceptable level of risk, while minimizing the expected

contributions and pension and postretirement expense.

In the optimization study, the Plan Administrator formulates

assumptions about characteristics, such as expected asset class invest-

ment returns, volatility (risk), and correlation coefficients among the

various asset classes. The future market assumptions used in the opti-

mization study are determined by examining historical market

characteristics of the various asset classes, and making adjustments to

reflect future conditions expected to prevail over the study period.

The optimization analysis utilized in the Plan Administrator’s latest

study produced the following approved asset class target allocations.

Pension Postretirement

Domestic Equity Securities 45% 37%

International Equity Securities 20% 14%

Fixed-Income Securities 31% 49%

Other (Cash and GACs) 4% 0%

These allocation percentages combined with each asset class’

expected investment return produced an aggregate return expectation

for the five years following the study of 7.6% for pension assets, 5.4%

for taxable postretirement assets, and 7.2% for non-taxable postretire-

ment assets.

The expected long term rate of return of 8.50% for the qualified

Retirement Plans assets is based on the expected return of each asset

class, weighted by the target allocation for each class. The expected

return for each asset class was developed using risk and return assump-

tions that use forward projections based on historical experience. This

analysis resulted in a weighted mean of 8.57% and a 50th percentile

return of 8.54% which supports the long term rate of return assump-

tion of 8.50%.

The expected long term rate of return of 8.50% for the non-taxable

VEBA trust assets is based on the expected return of each asset class,

weighted by the target allocation for each class. The expected return

for each asset class was developed using risk and return assumptions

that use forward projections based on historical experience. This

analysis resulted in a weighted mean of 8.24% and a 50th percentile

return of 8.22% which is consistent with the long term rate of return

assumption of 8.50%. For the taxable VEBA trust, the asset allocation

has a high percentage of non-taxable bonds. After reflecting the non-

taxable bond percentage and unrelated business income tax supports

an expected long term rate of return of 5.50%.

Since precise allocation targets are inefficient to manage security

investments, the following ranges were established to produce an

acceptable economically efficient plan to manage to targets:

Pension Postretirement

Domestic Equity Securities 45% to 55% 32% to 42%

International Equity Securities 15% to 25% 9% to 19%

Fixed-Income Securities 25% to 35% 44% to 54%

Other 0% to 10% 0% to 5%

ACCUMULATED PENSION BENEFIT OBLIGATION

The accumulated benefit obligation for Entergy’s qualified pension

plans was $2.7 billion and $2.5 billion at December 31, 2006 and

2005, respectively.

NOTESto CONSOLIDATED FINANCIAL STATEMENTS continued

85