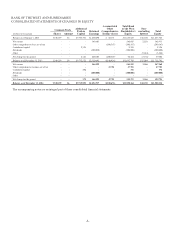

Bank of the West 2014 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2014 Bank of the West annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

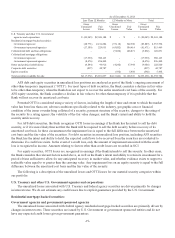

For derivatives designated as a cash flow hedge, in which derivatives hedge the variability of cash flows related to

floating-rate assets and liabilities or forecasted transactions, the accounting treatment depends on the effectiveness of the

hedge. To the extent that the hedge is considered effective in offsetting the variability of the hedged cash flows, changes in

the fair value of the derivative instrument are recorded in AOCI. These changes in fair value are subsequently reclassified

into consolidated statements of income in future periods when the hedged transaction affects earnings. To the extent the

derivative instruments are not effective, any changes in the fair value of derivatives are immediately recognized in

noninterest income. If a hedged forecasted transaction is not expected to occur or the derivative is no longer effective or

expected to be effective in offsetting changes in fair value or cash flows of a hedged item, hedge accounting is ceased.

For free-standing derivative instruments, any changes in the fair value of the derivative instruments are reported in

noninterest income.

The Bank occasionally purchases or originates financial instruments that contain embedded features that may

require recognition as separate derivative instruments. Such embedded derivatives are separated from the hybrid

financial instruments and are carried at fair value with any changes in fair value recorded in income for the current

period.

Valuations of derivative assets and liabilities reflect the value of the instrument including the values associated with

counterparty risk, market risk and the Bank’s own credit standing. See Note 14 for additional information.

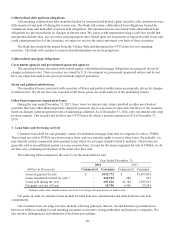

Recent accounting standards

The following Accounting Standard Updates (“ASU”) have been issued by the Financial Accounting Standards

Board (“FASB”) and are applicable to the Bank for the year ended December 31, 2014 or in future periods but are not

yet effective:

ASU 2014-01: Investments – Equity Method and Joint Venture (Topic 323) – Accounting for Investments in

Qualified Affordable Housing Projects

In January 2014, the FASB amended the guidance on the accounting for investments in qualified affordable housing

projects by removing the effective yield method and introducing a relatively less restrictive proportional amortization

method if certain criteria are met. The use of proportional amortization method for investments that qualify is an

accounting policy election. Under the proportional amortization method, an entity is allowed to amortize the cost of its

investments, in proportion to the tax credits and other tax benefits it receives, and present the amortization as a

component of income tax expense. The amended guidance is effective for the Bank’s 2015 annual reporting period. The

Bank has not elected the proportional amortization method as its accounting policy for future investments.

ASU 2014-04: Receivables – Troubled Debt Restructurings by Creditors (Subtopic 310-40) – Reclassification of

Residential Real Estate Collateralized Consumer Mortgage Loans Upon Foreclosure

In January 2014, the FASB issued guidance clarifying when a bank should reclassify mortgage loans collateralized

by residential real estate properties from the loan portfolio to OREO. The guidance specifies that a foreclosure or an in

substance repossession has occurred when either of the following criteria is met: (1) the creditor obtains legal title to the

residential real estate property upon completion of a foreclosure or; (2) the borrower conveys all interest in the

residential real estate property to the creditor to satisfy that loan through completion of a deed in lieu of foreclosure or

through a similar legal agreement. The guidance also requires new disclosures relating to foreclosed and repossessed

assets held by the Bank as well as loans in process of foreclosure according to local requirements of the applicable

jurisdiction. This guidance is effective for the Bank’s 2015 annual reporting period and may be applied either

prospectively or on a modified retrospective approach. The adoption of this guidance is not expected to have a material

impact on the Bank’s consolidated financial statements.

ASU 2014-08: Presentation of Financial Statements (Topic 205) and Property, Plant and Equipment (Topic 360) –

Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

In April 2014, the FASB issued guidance that changes the threshold for a disposal to qualify as a discontinued

operation and requires new disclosures of both discontinued operations and certain other disposals that do not meet the

definition of a discontinued operation. The new guidance is effective for the Bank’s 2015 annual reporting period and is

applied prospectively. The adoption of this new accounting guidance is not expected to have a material impact on the

Bank’s consolidated financial statements.

-15-