Albertsons 2005 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2005 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88

|

|

SUPERVALU INC. and Subsidiaries

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

including hedge funds, private equity and real estate are also used judiciously to enhance risk adjusted long-term

returns while improving portfolio diversification. The overall investment strategy and policy has been developed

based on the need to satisfy the long-term liabilities of the company’s pension plans. Risk management is

accomplished through diversification across asset classes, multiple investment manager portfolios and both

general and portfolio-specific investment guidelines. Risk tolerance is established through careful consideration

of the plan liabilities, plan funded status and the company’s financial condition. This asset allocation policy mix

is reviewed annually and actual allocations are rebalanced on a regular basis.

Plan assets are invested using a combination of active and passive investment strategies. Passive strategies

invest in broad sectors of the market primarily through the use of indexing. Indexing is an investment

management approach based on investing in exactly the same securities, in the same proportions, as an index,

such as the S&P 500. The management style is considered passive because portfolio managers don’t make

decisions about which securities to buy and sell, they simply mimic the composition and weightings of the

appropriate stock or bond market index. Active strategies employ multiple investment management firms.

Managers within each asset class cover a range of investment styles and approaches and are combined in a way

that controls for capitalization, and style biases (equities), and interest rate bets (fixed income) versus benchmark

indices while focusing primarily on issue selection as a means to add value. Monitoring activities to evaluate

performance against targets and measure investment risk take place on an ongoing basis through annual liability

measurements, periodic asset/liability studies and quarterly investment portfolio reviews.

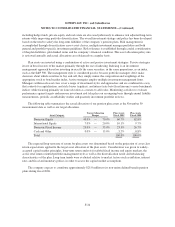

The following table summarizes the actual allocation of our pension plan assets at the November 30

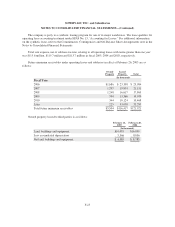

measurement date as well as our target allocation.

Asset Category

Target Allocation

Ranges

Plan Assets

Fiscal 2005

Plan Assets

Fiscal 2004

Domestic Equity 45.0% — 70.0% 60.7% 62.8%

International Equity 7.0% — 20.0% 10.1% 9.7%

Domestic Fixed Income 25.0% — 35.0% 23.5% 26.7%

Cash and Other 0.0% — 15.0% 5.7% 0.8%

Total 100.0% 100.0%

The expected long-term rate of return for plan assets was determined based on the projection of asset class

return expectations applied to the target asset allocation of the plan assets. Consideration was given to widely-

accepted capital market principles, long-term return analysis for global fixed income and equity markets, the

active total return oriented portfolio management style as well as the diversification needs and rebalancing

characteristics of the plan. Long-term trends were evaluated relative to market factors such as inflation, interest

rates and fiscal and monetary polices in order to assess the capital market assumptions.

The company expects to contribute approximately $25.0 million to its non-union defined benefit pension

plans during fiscal 2006.

F-34