Albertsons 2005 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2005 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

as well as the assumptions to be used in such models. The company plans to adopt the revised statement in its

first quarter of its fiscal year 2007, which begins on February 26, 2006.

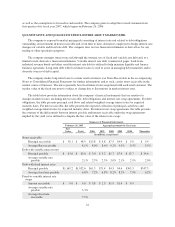

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

The company is exposed to market pricing risk consisting of interest rate risk related to debt obligations

outstanding, its investment in notes receivable and, from time to time, derivatives employed to hedge interest rate

changes on variable and fixed rate debt. The company does not use financial instruments or derivatives for any

trading or other speculative purposes.

The company manages interest rate risk through the strategic use of fixed and variable rate debt and, to a

limited extent, derivative financial instruments. Variable interest rate debt (commercial paper, bank loans,

industrial revenue bonds and other variable interest rate debt) is utilized to help maintain liquidity and finance

business operations. Long-term debt with fixed interest rates is used to assist in managing debt maturities and to

diversify sources of debt capital.

The company makes long-term loans to certain retail customers (see Notes Receivable in the accompanying

Notes to Consolidated Financial Statements for further information) and as such, carries notes receivable in the

normal course of business. The notes generally bear fixed interest rates negotiated with each retail customer. The

market value of the fixed rate notes is subject to change due to fluctuations in market interest rates.

The table below provides information about the company’s financial instruments that are sensitive to

changes in interest rates, including notes receivable, debt obligations and interest rate swap agreements. For debt

obligations, the table presents principal cash flows and related weighted average interest rates by expected

maturity dates. For notes receivable, the table presents the expected collection of principal cash flows and

weighted average interest rates by expected maturity dates. For interest rate swap agreements, the table presents

the estimate of the differentials between interest payable and interest receivable under the swap agreements

implied by the yield curve utilized to compute the fair value of the interest rate swaps.

Summary of Financial Instruments

February 26, 2005 Aggregate payments by fiscal year

Fair

Value Total 2006 2007 2008 2009 2010 Thereafter

(in millions, except rates)

Notes receivable

Principal receivable $ 50.1 $ 48.9 $13.8 $ 9.8 $7.5 $4.9 $ 3.0 $ 9.9

Average Rate receivable 8.1% 8.0% 8.6% 9.2% 9.9% 9.5% 5.5%

Debt with variable interest rates

Principal payable $ 63.6 $ 63.6 $ 3.0 $ 3.2 $1.7 $7.4 $ 13.7 $ 34.6

Average variable rate

payable 2.1% 2.5% 2.5% 3.0% 2.1% 2.1% 2.0%

Debt with fixed interest rates

Principal payable $1,169.2 $1,052.6 $61.3 $71.4 $4.5 $4.6 $363.3 $547.5

Average fixed rate payable 6.8% 7.2% 6.8% 8.2% 8.2% 7.9% 6.2%

Fixed-to-variable interest rate

swaps

Amount receivable $ 9.6 $ 9.6 $ 3.8 $ 2.3 $1.9 $1.4 $ 0.3

Average variable rate

payable 5.3%

Average fixed rate

receivable 7.9%

22