Albertsons 2005 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2005 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88

|

|

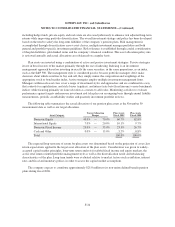

SUPERVALU INC. and Subsidiaries

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

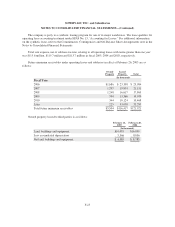

Pension Benefits Post Retirement Benefits

2005 2004 2003 2005 2004 2003

(In thousands)

NET BENEFIT COSTS FOR THE FISCAL

YEAR

Service cost $ 19,370 $ 18,243 $ 18,333 $ 1,443 $ 1,350 $ 1,790

Interest cost 37,957 35,003 33,228 6,899 7,457 7,336

Expected return on plan assets (41,843) (40,970) (40,323) — — —

Amortization of:

Unrecognized net loss 18,895 7,898 2,085 3,722 3,305 2,744

Unrecognized prior service cost 1,261 1,106 (158) (1,949) (1,200) (1,200)

Net benefit costs for the fiscal year $ 35,640 $ 21,280 $ 13,165 $10,115 $10,912 $10,670

In March 2003, the company amended its post retirement medical health care benefit plan, primarily making

changes to benefit coverage. This amendment resulted in a decrease in the plan’s benefit obligation of

approximately $4.5 million in fiscal 2004.

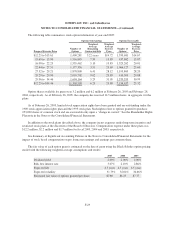

The company utilized the following assumptions in the calculations for pension and the non-contributory

unfunded pension plans:

2005 2004 2003

Weighted-average assumptions used to determine benefit

obligations:

Discount rate 6.00% 6.25% 7.00%

Rate of compensation increase 3.00% 3.00% 3.25%

Weighted-average assumptions used to determine net periodic

benefit cost:

Discount rate 6.25% 7.00% 7.25%

Rate of compensation increase 3.00% 3.25% 3.50%

Expected return on plan assets 8.75% 9.00% 9.25%

The assumed health care cost trend rate used in measuring the accumulated post retirement benefit obligation

was 12.0 percent in fiscal 2005. The assumed health care cost trend rate will decrease by one percent each year for

the next seven years until it reaches the ultimate trend rate of 5.0 percent. The health care cost trend rate assumption

has a significant impact on the amounts reported. For example, a one percent increase in the trend rate would

increase the accumulated post retirement benefit obligation by approximately $11 million and the service and

interest cost by approximately $1 million in fiscal 2005. In contrast, a one percent decrease in the trend rate would

decrease the accumulated post retirement benefit obligation by approximately $10 million and the service and

interest cost by approximately $1 million in fiscal 2005.

The company also maintains non-contributory unfunded pension plans to provide certain employees with

pension benefits in excess of limits imposed by federal tax law. The projected benefit obligation of the unfunded

plans was $18.1 million and $24.9 million at February 26, 2005 and February 28, 2004, respectively. The

accumulated benefit obligation of these plans totaled $14.2 million and $21.0 million at February 26, 2005 and

February 28, 2004, respectively. Net periodic pension cost was $3.6 million, $3.6 million and $2.7 million for

fiscal 2005, 2004 and 2003, respectively.

The company employs a total return approach whereby a mix of equities and fixed income investments are

used to maximize the long-term return of plan assets for a prudent level of risk. Alternative investments,

F-33