Albertsons 2005 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2005 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

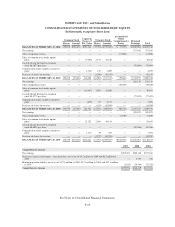

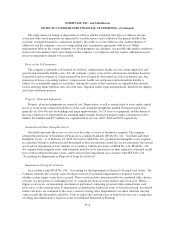

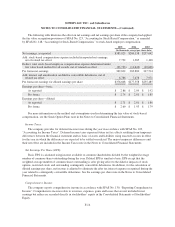

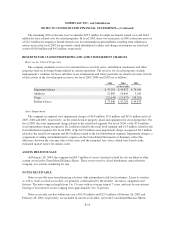

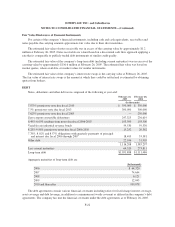

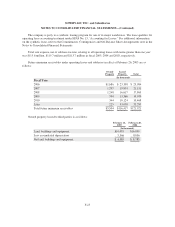

SUPERVALU INC. and Subsidiaries

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Use of Estimates:

The preparation of consolidated financial statements in conformity with accounting principles generally

accepted in the United States of America requires management to make estimates and assumptions that affect the

reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the

financial statements and the reported amounts of revenues and expenses during the reporting period. Actual

results could differ from those estimates.

Reclassifications:

Certain reclassifications have been made to conform prior years’ data to the current presentation. These

reclassifications had no effect on reported earnings.

New Accounting Standards

In January 2003, the Financial Accounting Standards Board (FASB) issued FASB Interpretation No. (FIN)

No. 46, “Consolidation of Variable Interest Entities” (FIN 46), and revised it in December 2003. FIN 46

addresses how a business should evaluate whether it has a controlling financial interest in an entity through

means other than voting rights and accordingly should consolidate the entity. FIN 46 applied immediately to

entities created after January 31, 2003, and no later than the end of the first reporting period that ended after

December 15, 2003 to entities considered to be special-purpose entities (SPEs). FIN 46 was effective for all other

entities no later than the end of the first interim or annual reporting period ending after March 15, 2004. The

adoption of the provisions of FIN 46 relative to SPEs and for entities created after January 31, 2003 did not have

an impact on the company’s consolidated financial statements. The other provisions of FIN 46 did not have an

impact on the company’s consolidated financial statements.

In December 2003, the FASB issued SFAS No. 132 (Revised 2003), “Employers’ Disclosures about

Pensions and Other Post Retirement Benefits—An Amendment of FASB Statements No. 87, 88 and 106.” This

statement increases the existing disclosure requirements by requiring more details about pension plan assets,

benefit obligations, cash flows, benefit costs and related information. The effect of the revisions to SFAS No. 132

is included in the Benefit Plan note in the Notes to Consolidated Financial Statements.

In May 2004, the FASB issued Financial Staff Position (FSP) No. 106-2, “Accounting and Disclosure

Requirements Related to the Medicare Prescription Drug, Improvement and Modernization Act of 2003.” FSP No.

106-2 supersedes FSP No. 106-1, “Accounting and Disclosure Requirements Related to the Medicare Prescription

Drug, Improvement and Modernization Act of 2003,” and provides guidance on the accounting and disclosures

related to the Medicare Prescription Drug, Improvement and Modernization Act of 2003 (the Medicare Act) which

was signed into law in December 2003. Except for certain nonpublic entities, FSP 106-2 is effective for the first

interim or annual period beginning after June 15, 2004. The company adopted FSP 106-2 in the second quarter of

fiscal 2005 using the retroactive application method and the fiscal 2005 impact was immaterial to the consolidated

financial statements. Based upon current guidance around the definition of actuarially equivalent, equivalence was

only determined with respect to a portion of the plan participants depending on plan benefits provided. If additional

clarifying regulations related to the Medicare Act or the definition of actuarially equivalent becomes available,

remeasurement of the plan obligations may be required, and related impacts on net periodic benefit costs would be

reflected prospectively in the consolidated financial statements.

In November 2004, the FASB ratified the effective date of the Emerging Issues Task Force (EITF)

consensus on Issue No. 04-8, “The Effect of Contingently Convertible Instruments on Diluted Earnings per

Share” to be applied to reporting periods ending after December 15, 2004. Under EITF Issue No. 04-8, net

earnings and diluted shares outstanding, used for diluted earnings per share calculations, are restated using the

if-converted method of accounting to reflect the contingent issuance of 7.8 million shares under the company’s

F-17