Tyson Foods 1999 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 1999 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

|

|

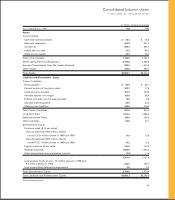

Notes to consolidated financial statements

TYSON FOODS, INC. 1999 ANNUAL REPORT

49

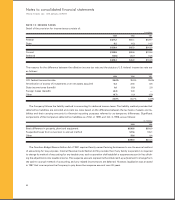

NOTE 9: LONG-TERM DEBT

The Company has an unsecured revolving credit agreement totaling $1 billion that supports the Company’s commercial

paper program. This $1 billion facility expires in May 2002. At Oct. 2, 1999, $290.5 million in commercial paper was out-

standing under this facility.

At Oct. 2, 1999, the Company had outstanding letters of credit totaling approximately $112.6 million issued primarily

in support of workers’ compensation insurance programs, industrial revenue bonds and the leveraged equipment loans.

Under the terms of the leveraged equipment loans, the Company had restricted cash totaling approximately $47mil-

lion which is included in other assets at Oct. 2, 1999. Under these leveraged loan agreements, the Company entered into

interest rate swap agreements to effectively lock in a fixed interest rate for these borrowings.

Annual maturities of long-term debt for the five years subsequent to Oct. 2, 1999, are: 2000 – $222.7 million; 2001 –

$142.9 million; 2002 – $321.1 million; 2003 – $177.8 million and 2004 – $29.2 million.

The revolving credit agreement and notes contain various covenants, the more restrictive of which require mainte-

nance of a minimum net worth, current ratio, cash flow coverage of interest and fixed charges and a maximum total

debt-to-capitalization ratio. The Company was in compliance with these covenants at fiscal year end.

Industrial revenue bonds are secured by facilities with a net book value of $69.5 million at Oct. 2, 1999. The weighted

average interest rate on all outstanding short-term borrowing was 5.5% at Oct. 2, 1999, and Oct. 3, 1998.

Long-term debt consists of the following:

in millions

Maturity 1999 1998

Commercial paper (5.9% effective rate at 10/2/99) 2002 $«««290.5 $÷«506.9

Debt securities:

6.75% notes 2005 149.5 149.3

6.625% notes 2005 149.6 149.5

6.39-6.41% notes 2000 50.0 50.0

6% notes 2003 147.7 146.8

7% notes 2028 146.3 145.9

7% notes 2018 236.5 236.3

Institutional notes:

10.61% notes 1999-2001 53.1 106.3

10.84% notes 2002-2006 50.0 50.0

11.375% notes 1999-2002 8.5 12.8

Mandatory Par Put Remarketed Securities

(5.5% effective rate at 10/2/99) 2010 0.1 50.2

6.08% notes 2010 0.1 100.4

Leveraged equipment loans (rates ranging from 4.7% to 6.0%) 2005-2008 154.5 170.5

Other various 78.8 91.7

$1,515.2 $1,966.6