Tyson Foods 1999 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 1999 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

Notes to consolidated financial statements

TYSON FOODS, INC. 1999 ANNUAL REPORT

44

On July 17, 1999, the Company completed the sale of the assets of Tyson Seafood Group in two separate transactions.

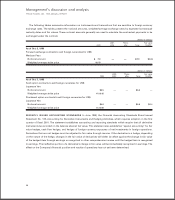

Under the terms of the agreements, the Company received proceeds of approximately $165 million, which was used to

reduce indebtedness, and subsequently collected receivables totaling approximately $16 million. The Company recog-

nized a pretax loss of approximately $19.2 million on the sale of the seafood assets.

Effective Dec. 31, 1998, the Company sold Willow Brook Foods, its integrated turkey production and processing busi-

ness, and its Albert Lea, Minn., processing facility which primarily produced sausages, lunch and deli meats. In addition,

on Dec. 31, 1998, the Company sold its National Egg Products Company operations in Social Circle, Ga. These facilities

were sold for amounts that approximated their carrying values. These operations, which were reflected in assets held for

sale at Oct. 3, 1998, were acquired as part of the acquisition of Hudson Foods, Inc. (Hudson or Hudson Acquisition) in

January 1998. The remaining balance of assets held for sale at Oct. 3, 1998, relates to facilities identified for closing under

the Company’s restructuring program which are expected to be disposed of within the next 12 months.

Effective Nov. 25, 1996, the Company sold its beef further-processing operations, known as Gorges/Quik-to-Fix Foods,

resulting in a pretax gain of $41 million which was recorded in other income for fiscal 1997 in the Consolidated Statements

of Income. The operating results of this facility were not material to the Company in 1997.

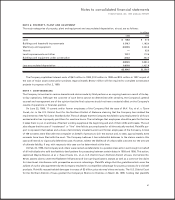

NOTE 3: ACQUISITIONS

On Jan. 9, 1998, the Company completed the acquisition of Hudson Foods, Inc. At the effective time of the acquisition,

the Class A and Class B shareholders of Hudson received approximately 18.4 million shares of the Company’s Class A

common stock valued at approximately $363.5 million and approximately $257.4 million in cash. The Company borrowed

funds under its commercial paper program to finance the cash portion of the Hudson Acquisition and repay approxi-

mately $61 million under Hudson’s revolving credit facilities. The Hudson Acquisition has been accounted for as a

purchase and the excess of investment over net assets acquired is being amortized straight-line over 40 years. The

Company’s consolidated results of operations include the operations of Hudson since the acquisition date. The follow-

ing unaudited pro forma information shows the results of operations as though the purchase of Hudson had been made

at the beginning of fiscal 1997.

in millions, except per share data

1998 1997

Net sales $7,831.0 $8,020.8

Net income 16.8 140.3

Basic Earnings Per Share 0.07 0.60

Diluted Earnings Per Share $÷÷«0.07 $÷÷«0.59

The unaudited pro forma results are not necessarily indicative of the actual results of operations that would have

occurred had the purchase actually been made at the beginning of 1997, or the results that may occur in the future.

NOTE 4: IMPAIRMENT AND OTHER CHARGES

In July 1999, the Company signed a letter of intent to sell Mallard’s Food Products (Mallard’s) for an amount less than

net book value. The sale of Mallard’s was not consummated. However, based upon these negotiations and the Company’s

cash flow projections, management believes that certain long-lived assets and related excess of investments over net

assets acquired are impaired. The Company recorded in the fourth quarter of 1999 pretax charges totaling $22.5 million

($0.10 per share) for impairment of property and equipment and write-down of related excess of investments over net

assets acquired of Mallard’s. Management expects that Mallard’s will continue to be a part of the Prepared Foods Group.